Current Problems

67% of investors generate lower returns than the index

Investors earn 5.8% less than their mutual funds over a 10-year period

Over 50% of portfolios are Over Diversified

Solutions We Offer

Optimized Allocation

We help you diversify strategically and avoid overlaps by optimizing asset allocation and sector selection.

Proactive Management

We monitor market trends and help rebalance your portfolio for sustained growth.

Discover Hidden Gems

We identify high-potential, lesser-known funds with the ability to outperform mainstream options.

Dedicated Guidance

Get personalized updates and insights from your relationship manager. Our advisors have over 25+ years of experience in portfolio constructing.

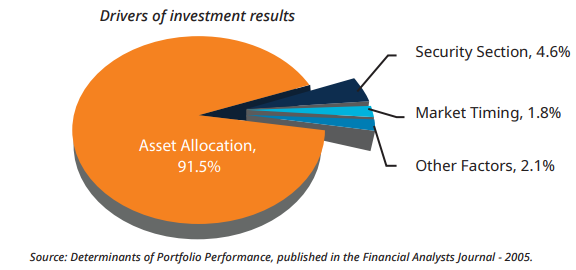

What Drives Investment Outcomes?

Investors often focus too much on selecting the best-performing stocks/schemes.

Historical analysis shows that asset allocation is the primary factor influencing portfolio performance.

A well-diversified allocation strategy drives consistent long-term returns.

How to generate Alpha (α)?

1

MCAP SELECTION

We balance large, mid, and small caps to enhance risk-adjusted returns

2

SECTOR SELECTION

We identify trends early and guide investors in sector rotation to optimize returns.

3

FUND SELECTION

We pick high-quality funds with strong track records and efficient management.

We may not always get market timing right, but we ensure the right asset selection, sector rotation, and fund choices to optimize returns.

What Our Customers Say

Schedule a call with our experts

- Free Portfolio Review

- Goal-Based Planning

- Expert Recommendations

Did You Know?

Indian equities have given approx 14% returns over 20 years.

Mutual funds have outperformed indexes and given aaprox. 15% to 19% returns over 20 years.

Which means your money would have multiplied 15 to 20X in 20 years.

Featured Blogs

F.A.Q

-

When were Mutual Funds introduced in India?

Mutual funds in India began in 1963 with the Unit Trust of India (UTI), backed by the Government of India and RBI. The first scheme, US-64, launched in 1964, gained immense popularity. In 1987, public sector banks and institutions entered the industry, with SBI launching the first non-UTI fund. The 1991 economic liberalization allowed private players, increasing competition and innovation. SEBI, established in 1992, became the industry regulator. By September 2023, the industry’s AUM had grown to ₹46.58 trillion, with 44 AMCs operating in the market.

-

What is NAV in a Mutual Fund, and how is it calculated?

NAV (Net Asset Value) is the per-unit price of a mutual fund, calculated as: NAV = (Total Assets - Total Liabilities) / Total Number of Outstanding Units For example, if a fund has ₹10,00,000 in assets, ₹50,000 in liabilities, and 1,00,000 units, the NAV would be ₹9.5. NAV is updated daily based on the closing prices of the fund’s holdings

-

What is an Asset Management Company (AMC)?

An AMC manages mutual fund schemes by pooling investor money and investing in various securities. Fund managers make investment decisions, handle compliance, and track fund performance. AMCs charge an expense ratio for management and operational costs. They are regulated by SEBI to ensure transparency. Top AMCs include SBI MF, ICICI MF, HDFC MF, and Axis MF.

-

What is the Expense Ratio in a Mutual Fund?

The expense ratio is the annual cost of managing a fund, expressed as a percentage of AUM. For example, a 1.5% expense ratio means ₹1.5 is charged annually per ₹100 invested. SEBI sets limits: equity funds can charge up to 2.25%, while debt funds have a 2.0% cap. A lower expense ratio helps maximize investor returns.

-

How are Mutual Fund Returns Calculated?

- Absolute Return: Simple percentage change in NAV over time.

- CAGR (Compound Annual Growth Rate): Annualized return accounting for time.

- TWRR (Time-Weighted Rate of Return): Adjusts for multiple cash flows but ignores size.

- XIRR (Extended Internal Rate of Return): Considers both cash flow timing and size, offering the most comprehensive measure.

-

What is Exit Load in a Mutual Fund?

Exit load is a fee charged if investors redeem units before a specified period. For example, a 1% exit load on a ₹10,000 redemption means a ₹100 deduction. It discourages early withdrawals.

-

How to Choose a Mutual Fund?

Select a fund based on:

- Investment Horizon: Equity funds for long-term goals (5+ years), debt/hybrid for shorter periods.

- Performance vs. Benchmark: Active funds should consistently outperform; passive funds should have low tracking error.

- Expense Ratio: Compare within the same category.

- Risk Profile: Consider asset allocation and debt fund credit quality. Regular monitoring ensures alignment with financial goals.

-

Who is a Mutual Fund Manager?

A fund manager oversees investment decisions, portfolio allocation, and market analysis to achieve fund objectives.

- Active Managers: Aim to outperform benchmarks, leading to higher expense ratios.

- Passive Managers: Track indices, focusing on minimizing tracking error.

-

Can Investors Lose Money in Mutual Funds?

Yes, due to market fluctuations, fund misalignment with investor goals, or poor management. For instance, sectoral funds face higher risks if their sector underperforms. Staying invested through market downturns can mitigate losses.

-

What Charges Apply to Mutual Fund Investments?

- Expense Ratio: Management fees deducted annually.

- Stamp Duty & STT: 0.005% on purchases, 0.001% on redemptions (equity funds).

- Capital Gains Tax: 20% for short-term (<1 year), 12.5% for long-term (>1 year, above ₹1.25 lakh gains).

- Exit Load: If applicable, varies by fund.

- Dividend Taxation: Taxed as per the investor’s income slab.

-

Can I Invest in Mutual Funds for My Child (Minor)?

Yes, a parent/guardian can invest on behalf of a minor. A separate account is required, with the guardian managing it until the child turns 18. On turning 18, KYC needs to be completed for account transfer. Returns are clubbed with the guardian’s income.

-

Can Mutual Funds Be Held in a Joint Account?

Yes, joint mutual fund accounts are allowed for shared financial goals. All holders must complete KYC, and transactions typically require approval from all account holders.

-

What is a New Fund Offering (NFO)?

An NFO is the launch of a new mutual fund by an AMC, offered at a fixed price (usually ₹10 per unit). Similar to an IPO, it helps raise capital for investments. Investors should assess the fund’s theme and objectives before investing.

-

Difference Between ETFs and Mutual Funds

Both pool investor money, but ETFs trade on exchanges like stocks, with prices fluctuating throughout the day. Mutual funds are bought/sold at NAV, calculated at day’s end. ETFs are mostly passive and cost-effective, while mutual funds can be actively managed but carry higher fees. ETFs are also more tax-efficient.

-

SIP vs. Lump Sum Investment

SIP spreads investments over time, averaging costs and reducing market timing risks—ideal for steady earners. Lump sum investments suit those confident in market trends but carry higher risk.

-

Mutual Fund Redemption Timeline

Equity funds settle in T+3 days, debt funds in T+2 days. Processing may be delayed on weekends/holidays, with proceeds credited to your bank account.

-

Can HUFs Invest in Mutual Funds?

Yes. A HUF can invest using its own PAN and bank account. The Karta, as the head, must complete non-individual KYC with documents like PAN, bank statement, and HUF declaration deed.

-

Mutual Fund Taxation

Tax depends on the fund type and holding period: Equity Mutual Funds

- Sold before July 23, 2024: STCG @ 15%, LTCG @ 10%

- Sold after July 23, 2024: STCG @ 20%, LTCG @ 12.5%

- Invested before April 1, 2023:

- Sold before July 23, 2024: LTCG (held > 36 months) @ 20% with indexation, STCG taxed per slab

- Sold after July 23, 2024: LTCG (held > 24 months) @ 12.5% with indexation, STCG taxed per slab

- Invested after April 1, 2023: Taxed as per income slab, regardless of holding period.

India's most trusted Platform for Buying and Selling Unlisted Shares

Social Media

Join our WhatsApp Community

Altius Investech

Altius Investech Private Limited

Download Our App

Startup India Certificate No.

DIPP43865

CIN No.

U74900WB2016PTC210376