India’s organised retail market is only 18% of total retail. That number, small as it looks, represents a Rs. 190 lakh crore market by 2034. Three companies are fighting to define what that organised slice looks like. Their strategies could not be more different from each other. So could their investment stories.

1. The Big Picture: India’s Retail Opportunity

India’s total retail market is one of the largest in the world and one of the least penetrated by organised players. The share of organised retail constitutes just 18% of the total retail market, while the unorganised segment, characterised by millions of small kiranas, constitutes the remaining 82%. According to BCG and the Retailers Association of India, India’s retail sector is projected to reach Rs. 190 lakh crore by 2034, growing at a CAGR of 9%.

That unorganised 82% is the prize. It is also why Reliance, DMart, and Trent can all be growing at double-digit rates simultaneously without materially eating into each other’s core business yet. The market is still so large and so under-penetrated that the primary competition is not each other. It is inertia, kirana culture, and consumer habit.

But that is changing. As India urbanises, as digital payments reduce friction, as supply chains become more sophisticated, the organised players are beginning to overlap in ways they did not five years ago. Understanding each company’s model and where that overlap occurs is the central task for any investor in this space.

2. Reliance Retail: The Scale Machine

There is no analogy in Indian retail for what Reliance has built. Reliance leads in scale with 18,700-plus stores and Jio-backed expansion, posting Rs. 84,171 crore in a single quarter against DMart’s Rs. 16,359 crore. The sheer order-of-magnitude difference makes most head-to-head comparisons feel slightly absurd.

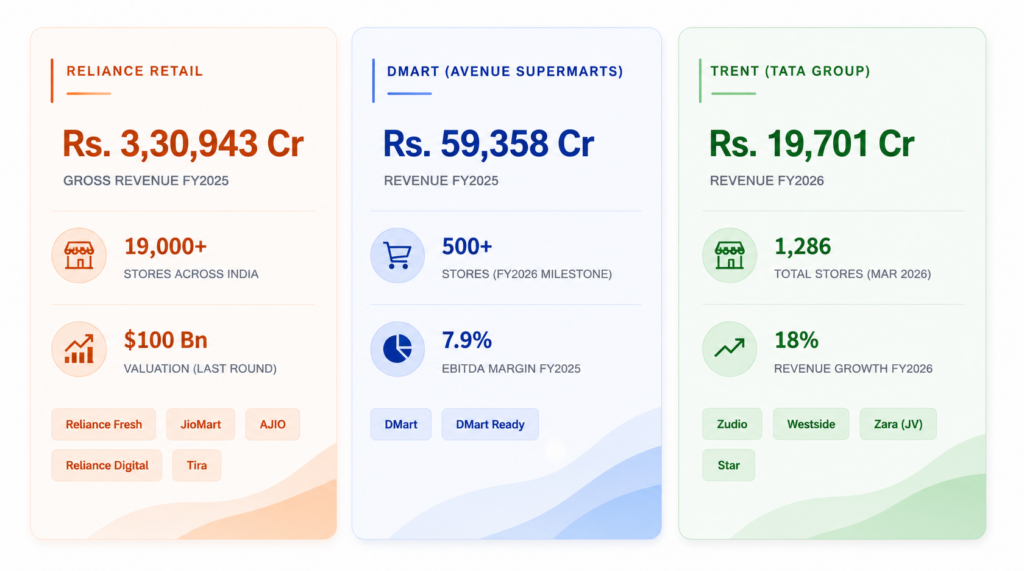

Reliance Retail is not one business. It is a portfolio of retail businesses spanning grocery (Reliance Fresh, Smart Bazaar), fashion and lifestyle (Reliance Trends, AJIO), electronics (Reliance Digital), jewellery (Reliance Jewels), pharmacy, and beauty (Tira). Reliance Retail recorded Gross Revenue of Rs. 3,30,943 crore for FY2025, a growth of 7.9% over the prior year.

The JioMart Integration Advantage

What separates Reliance from every other retail player in India is its ability to use the Jio digital infrastructure as a distribution engine. JioMart was initially mocked as an overly ambitious grocery play. It has since evolved into a multi-category platform that integrates kirana stores, Reliance’s own front-end stores, and a consumer-facing app into one logistics network. This “phygital” model, integrating physical and digital retail, positions Reliance not just as a retailer but as the infrastructure layer for India’s organised commerce transition.

The Unlisted Angle

Reliance Retail is one of the most discussed and widely sought names in India’s unlisted share market. Reliance Retail has raised significant funding from investors like Silver Lake, KKR, GIC, TPG, Qatar Investment Authority, and Abu Dhabi Investment Authority, achieving a valuation of $100 billion. This makes it India’s most valuable unlisted company by a considerable margin.

For pre-IPO investors, Reliance Retail represents a bet on India’s largest retail infrastructure play before it reaches public markets. The IPO, when it comes, will be one of the largest in Indian market history. Entry through the unlisted market, at current prices, is one of the few ways retail investors can access it ahead of that event.

Challenges Worth Noting

Revenue growth of 7.9% in FY2025 is below what analysts and investors had come to expect from a company at this stage of scale-building. The fashion segment faces pressure from Trent and Zudio. The grocery segment competes against DMart’s pricing discipline. Managing 19,000-plus stores across formats, geographies, and supply chains is operationally complex in ways that smaller, focused competitors do not face. Margin visibility across the consolidated entity is also limited given the multi-format, multi-segment structure.

3. DMart: The Efficiency Fortress Under Siege

DMart is one of the most studied retail success stories in India. Founded by Radhakishan Damani, it was built on a deceptively simple principle: own the real estate, keep costs below every competitor, pass those savings to customers, and earn volumes that compensate for thin margins. For two decades, this worked spectacularly.

DMart’s FY2025 revenue surged 16.7% year-on-year to Rs. 57,790 crore, while net profit rose 8.6% to Rs. 2,927 crore. The company added 50 new stores in FY2025, bringing its total to 415 stores across 10 states.

The trouble is what is happening at the margins. DMart’s EBITDA margin fell to 7.9% from 8.3% in FY2024, driven by rising costs in labour, FMCG competition, and investments in operational efficiency. For a business model built on wafer-thin margins and high volumes, even small margin compression is a meaningful structural signal.

The DMart Model: Why It Worked

DMart’s genius was its EDLC-EDLP strategy: Everyday Low Cost, Everyday Low Price. By owning rather than leasing store real estate (a capital-intensive but margin-protective decision), negotiating 30-day payment terms with suppliers versus the industry norm of 45-60 days, and maintaining a tight SKU count of around 5,000-6,000 lines (versus hypermarket competitors with 15,000+), DMart achieved consistent stock turns that generated returns on invested capital that were the envy of the global retail industry.

The Quick Commerce Problem

DMart’s stores are large-format, high-throughput, and concentrated in urban centres. This is precisely where quick commerce has done the most damage. DMart’s CEO Neville Noronha acknowledged in the company’s results: “We clearly see the impact of online grocery formats including DMart Ready in large metro DMart stores which operate at a very high turnover per square feet of revenue.”

The rapid proliferation of online grocery plays is hitting DMart’s high-turnover metro stores and may slow down same-store sales growth momentum, which is why there is a shift to locations in smaller towns. This is a material strategic pivot: DMart is moving expansion towards smaller cities and Tier 2-3 markets, where quick commerce penetration is lower and large-format stores still have a clear value proposition.

Emkay maintained a sell rating on DMart, citing slow total addressable market expansion, a fading USP on value and assortment versus quick commerce, deteriorating return on invested capital, and an expensive valuation at 80x one-year forward earnings.

The DMart investor dilemma: The business remains excellent in absolute terms. Revenue is growing at 15-17%. Stores are profitable. The balance sheet is debt-free. But the valuation at 80x forward earnings prices in a growth trajectory that quick commerce competition is actively disrupting. Growth is slowing from 30% to low teens. And the market has not fully priced that deceleration yet.

4. Trent: The Quiet Compounder That Surprised Everyone

If Reliance is the juggernaut and DMart is the efficiency machine, Trent is the surprise. A Tata Group company that most investors regarded as a competent but unremarkable fashion retailer for most of its existence, Trent has undergone a transformation over the past four years that has left analysts repeatedly revising their estimates upward.

The engine is Zudio. For the full financial year FY2026, Trent’s revenue rose 18% to Rs. 19,701 crore. In the March quarter alone, Trent added 109 Zudio stores and 22 Westside stores, taking its total store count to 1,286 outlets as of March 31, 2026, including 963 Zudio stores and 300 Westside outlets.

The Zudio Model: Value Fashion Done Differently

Zudio’s success comes from a combination of factors: rapid inventory turnover with fresh styles hitting shelves every few weeks, a focus on private-label sales limiting COGS to 60-65%, and smaller store sizes averaging 9,500 square feet compared to Westside’s 21,000 square feet. Revenue per square foot stands at Rs. 16,300, double the industry average.

Critically, Zudio has stayed away from two practices that damage most value fashion retailers: heavy discounting and active marketing spend. The annual report notes: “We instead focus on being accessible and building a critical mass of presence to drive awareness.” Zudio crossed $1 billion in sales in FY2025 with lifestyle and non-apparel accounting for over 20% of revenues.

The geographic strategy is also telling. Zudio’s aggressive expansion targeted smaller cities where real estate costs are significantly lower than metropolitan areas, enabling faster breakeven on new locations. This is precisely the direction DMart is now being forced to pivot toward, which means the two models are converging on the same geography from different starting points.

Westside: The Anchor That Gets Overlooked

In the excitement around Zudio, Trent’s Westside business often gets undersold. Westside is a mid-premium fashion retail brand with 300-plus stores, strong private label margins, a loyalty programme that drives repeat visits, and an online channel that grew volumes 41% in FY2025. It is profitable, cash-generative, and provides a stable anchor for the Trent portfolio.

The Trent compounding story in numbers: From under 90 Zudio stores in FY2021 to 963 by March 2026. Revenue growing at 18-20% annually. New store investment of Rs. 3-4 crore per Zudio outlet generating returns within 12-18 months. Each store opening is accretive from a relatively early stage, giving Trent one of the most capital-efficient expansion models in Indian retail.

5. Head-to-Head: Key Financials Compared

| Metric | Reliance Retail | DMart | Trent |

|---|---|---|---|

| Revenue (Most Recent Full Year) | Rs. 3,30,943 Cr (FY25) | Rs. 59,358 Cr (FY25) | Rs. 19,701 Cr (FY26) |

| Revenue Growth (YoY) | 7.9% | 16.7% | 18% |

| EBITDA Margin | Not separately disclosed | 7.9% (FY25) | ~11-12% (FY26 est.) |

| Store Count | 19,000+ | 500+ (FY26 milestone) | 1,286 (Mar 2026) |

| Store Addition Pace | Aggressive, multi-format | ~50-60 per year | 250-300 per year (Zudio-led) |

| Primary Formats | Grocery, fashion, electronics, beauty | Large-format hypermarket only | Value fashion, lifestyle fashion |

| Debt Position | Minimal (backed by RIL) | Debt-free (owned real estate) | Net cash positive |

| Listed Status | Unlisted (subsidiary of RIL) | Listed (NSE: DMART) | Listed (NSE: TRENT) |

| Key Risk | Complexity of scale; slower growth | Quick commerce disruption in metros | Sustaining growth on high base |

| Key Strength | Infrastructure depth, JioMart ecosystem | Owned real estate, margin discipline | Zudio capital efficiency, Tata brand |

6. The Quick Commerce Wildcard

No analysis of Indian organised retail in 2026 is complete without addressing quick commerce. Blinkit, Swiggy Instamart, and Zepto have collectively crossed Rs. 30,000 crore in annualised GMV. They are growing at 40-60% annually. And they are eating directly into the basket of grocery and FMCG products that once anchored DMart’s high-traffic metro stores.

The impact is not uniform across the three companies we are comparing.

DMart is the most exposed. Its large-format stores depend on customer trips for stocking up. When a household shifts even 20-30% of its grocery purchases to quick commerce, that is enough to materially affect same-store sales growth in affected catchments. DMart’s response, DMart Ready, exists but remains subscale and, by management’s own admission, far from standalone profitable.

Reliance is partly insulated and partly competing. JioMart and Reliance’s B2C quick delivery initiatives position it as both an incumbent and an aggressor in the fast-delivery space. Whether Reliance can convert its logistical infrastructure into a quick commerce winner remains to be seen, but the capability is there in a way DMart’s never was.

Trent is least exposed. Fashion retail is not a quick commerce category. Nobody uses Blinkit to buy a kurta. Zudio’s format has no meaningful competitive overlap with quick commerce, which is almost entirely focused on grocery, household, and FMCG. This structural insulation is an underappreciated advantage in the current environment.

7. The Investor Verdict

These three companies are not interchangeable. They represent three fundamentally different bets on India’s retail future. Here is how to think about each one.

Reliance Retail

- The pre-IPO bet: India’s most valuable unlisted company with the largest retail infrastructure

- Patient capital required: IPO timeline is not confirmed

- Upside case: JioMart + physical network integration delivers a flywheel no competitor can replicate

- Risk: Growth has decelerated; managing complexity at 19,000 stores is non-trivial

- Best for: Unlisted investors comfortable with 3-5 year horizons seeking India’s largest retail story

DMart

- The defensive compounder under pressure: excellent business, expensive valuation

- Quick commerce disruption in metros is real and management has acknowledged it

- Tier 2-3 expansion is the strategic pivot: lower competition, lower real estate cost

- Risk: 80x forward P/E leaves almost no room for growth disappointment

- Best for: Listed market investors who believe the quick commerce threat is overstated and the brand moat holds

Trent

- The growth compounder with the clearest near-term visibility

- Zudio’s unit economics are exceptional; store additions are accretive quickly

- No quick commerce exposure is a structural advantage right now

- Risk: Sustaining 18-20% growth on an Rs. 20,000 crore base requires relentless execution

- Best for: Listed investors looking for India’s best pure-play value fashion exposure

The one thing all three agree on: India’s organised retail penetration moving from 18% to 30-35% over the next decade is not a question of whether but when. Whichever of these three companies you pick, you are positioned for that structural tailwind. The debate is about which model captures the most of it, at which risk-adjusted price.

GET IN TOUCH WITH US

For any query or personal assistance, feel free to reach out at support@altiusinvestech.com or call us at +91-6289225026.

Learn more about Unlisted Companies and Pre-IPO opportunities at Altius Investech.

Join our LinkedIn Newsletter: The Market Buzz by Altius