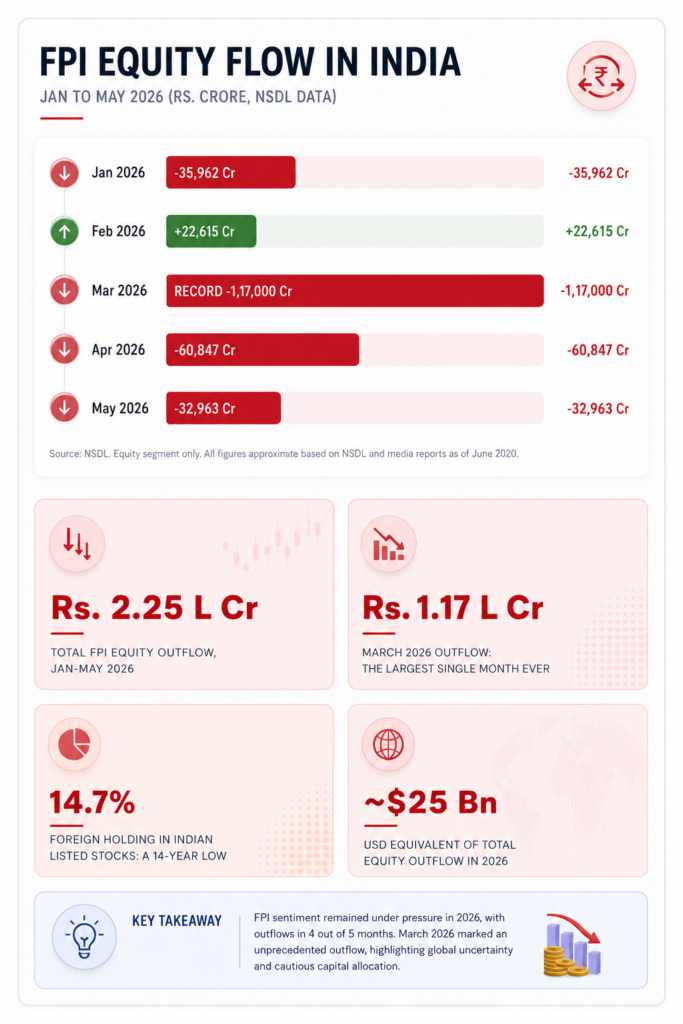

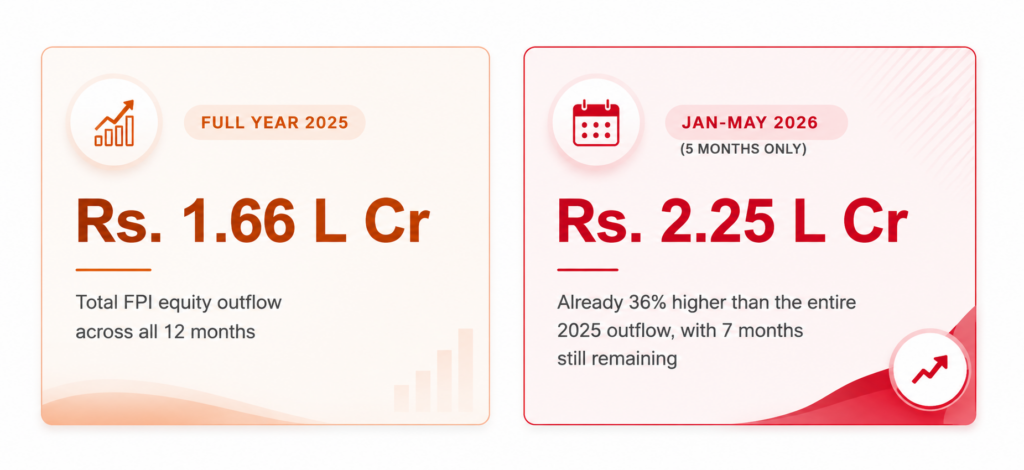

In the first five months of 2026, Foreign Portfolio Investors have pulled out Rs. 2.25 lakh crore from Indian equities. That is more than the entire Rs. 1.66 lakh crore they withdrew across all twelve months of 2025. One of those months, March 2026, was the largest single-month FPI outflow in the history of Indian capital markets. Here is the complete picture of what happened, why it happened, and what it tells us about India’s position in global capital flows.

1. The Numbers: Month by Month

The headline is dramatic enough. But the month-by-month breakdown reveals something even more striking: how abrupt the sentiment reversal was, and how concentrated the damage has been.

The February reversal deserves a mention. FPIs invested Rs. 22,615 crore in February 2026, the highest monthly inflow in 17 months. The market rallied. Analysts called it a turning point. Then March arrived and erased all of that optimism in a single record-breaking month of selling.

2. 2026 vs 2025: How This Compares

To understand how severe the 2026 situation is, it helps to look at the full 2025 FPI picture alongside it.

The 2025 outflow was itself historically large. The year saw heavy selling through most months, with a brief respite in October (Rs. 14,610 crore inflow) before selling resumed in November and December. Full year 2025 saw FPIs withdraw Rs. 1.66 lakh crore, which at the time was one of the largest annual outflows on record.

2026 has already exceeded that in five months.

To place it in the broadest historical context: one report described the pace of selling as the worst yearly number since 1993, when foreign portfolio investing in Indian equities was first permitted. The data is jarring, and the question of why it is happening deserves serious analysis.

3. The Six Reasons FPIs Are Selling India

There is no single cause for outflows of this scale. They reflect a confluence of global and India-specific factors that have aligned in an unusually negative way during this period.

Reason 1 :

The Rupee Is Falling, and Fast

Foreign investors receive their returns in dollars, not rupees. When the rupee weakens, every rupee of Indian equity return is worth fewer dollars when repatriated. The rupee has weakened nearly 6% so far in 2026 and approximately 10% over the past year, falling from the mid-80s to approximately 95.5 against the US dollar despite RBI’s efforts to defend the currency. At 96 rupees per dollar, a 20% gain in an Indian stock translates to a roughly 14% dollar-denominated return. That compression makes India less attractive relative to markets with stable currencies.

Reason 2 :

Crude Oil Is Surging and India Imports 80% of Its Requirements

Brent crude has moved from approximately $70 per barrel to $95-105 amid disruptions around the Strait of Hormuz driven by the US-Iran conflict. India imports more than 80% of its crude oil requirements, making it acutely vulnerable to oil price shocks. Higher oil means a larger import bill, a wider current account deficit, more pressure on the rupee, higher domestic inflation, and reduced monetary policy flexibility. It is a chain reaction that hits every part of the macro picture simultaneously.

Reason 3 :

India’s Earnings Growth Has Disappointed

FPIs are fundamentally investing in corporate earnings. When those earnings fail to keep pace with valuation, the case for holding weakens. India Inc.’s earnings growth has been disappointing relative to expectations through FY2025 and into FY2026. IT stocks, which represent a large chunk of FPI holdings, faced pressure from global enterprise tech spending caution. FMCG companies struggled with rural demand softness. The aggregate earnings picture did not justify the valuations at which India’s market was trading entering 2026, creating a fundamental reset pressure that ran alongside the macro headwinds.

Reason 4 :

US Interest Rates Staying Higher for Longer

When US treasury yields are elevated, the risk-free rate of return in the world’s deepest capital market is high. That raises the hurdle rate for emerging market equities. An investor who can earn 4.5-5% in US treasuries without taking any emerging market risk, currency risk, or liquidity risk requires a higher expected return from Indian equities to justify the additional risks. The yield differential between Indian and US government bonds remained below 2% for most of the year, a historically narrow spread that reduces the relative attractiveness of Indian fixed income and by extension Indian equities for global allocators.

Reason 5 :

US-India Tariff Uncertainty and Geopolitical Tensions

Trump’s reciprocal tariff announcements in early April 2026 triggered a sharp wave of selling across emerging markets. India was not immune. The uncertainty around the final tariff structure, potential trade agreement negotiations, and the India-Pakistan tensions in May 2026 created a risk environment that prompted risk reduction across global portfolios. India benefited from relative geopolitical stability for years. That premium has partially eroded as the regional risk picture has become more complex.

Reason 6 :

Better Opportunities Elsewhere

Capital is global. When FPIs reduce India exposure, they are often increasing exposure elsewhere. The Chinese government’s stimulus announcements in late 2024 and the resulting rally in Hong Kong and mainland Chinese equities pulled some global allocation capital away from India. US technology stocks, particularly AI infrastructure plays, have delivered extraordinary returns that have attracted capital that might otherwise have diversified into emerging markets. The FPI selling in India is partly an India story and partly a global rotation story.

4. Where Is the Money Going?

Understanding the flows requires understanding the alternatives that look more attractive to global allocators right now.

| Destination / Asset Class | Why It Is Attracting Capital Away from India |

|---|---|

| US AI Technology Stocks | SanDisk, Intel, Nvidia, and the broader AI semiconductor complex have delivered returns that dwarf any emerging market. Capital follows performance. |

| US Treasuries | 4.5-5% yield with zero credit risk. The risk-free rate is high enough to attract capital that previously sought emerging market equity premium. |

| Chinese Equities | Government stimulus and relatively lower valuations made Hong Kong and Shanghai attractive for rotation from expensive Indian equities. |

| Japanese Equities | The Nikkei’s multi-decade highs and a weak yen made Japan’s export-oriented companies highly attractive to global investors in 2025-26. |

| European Markets | Defence sector boom and energy infrastructure investment attracted capital following Russia-Ukraine and Middle East conflict escalation. |

5. The DII Buffer: India’s New Shock Absorber

The most important structural shift in India’s equity market over the past five years is that FPI selling no longer automatically means market collapse. The domestic institutional investor (DII) base, fed by a relentless monthly SIP inflow into mutual funds, has become large enough to partially absorb FPI selling and provide a floor under valuations.

Aggregate foreign holding in Indian listed stocks fell to a 14-year low of 14.7% during this selling wave. Domestic institutions’ holding simultaneously rose to 18.9%, higher than FPI holding for what is believed to be the first time. That is a historic structural shift in market ownership that would have been unthinkable a decade ago.

The SIP army in numbers: India’s monthly SIP inflow into equity mutual funds has been running above Rs. 25,000 crore per month consistently through 2025-26. That translates to approximately Rs. 3 lakh crore per year of systematic domestic equity buying, regardless of market levels, regardless of FPI sentiment, and regardless of global macro conditions. FPIs can sell. The SIP investor keeps buying. The two forces are increasingly balancing each other in a way that has changed the character of Indian equity market corrections.

This does not mean FPI outflows are irrelevant. They still move markets, still pressure the rupee, and still create buying opportunities for patient domestic investors. But the days when an FPI selling wave could produce a 40-50% market crash are gone, precisely because the domestic investor base now provides structural demand support on the other side.

6. What to Watch Going Forward

FPI flows are not fixed. They reverse. The same global factors that triggered the 2026 selling wave can reverse when conditions change. Here are the specific indicators to track.

Rupee Stabilisation

The rupee is the single most direct link between global macro conditions and FPI behaviour. RBI’s forex reserves stood at approximately $690 billion, but adjusting for gold holdings and short positions, effective import cover has fallen to about 5.8 months, the lowest since 2014. Any improvement in the rupee trajectory, driven by lower oil prices, improved current account, or RBI intervention, will quickly improve the calculus for dollar-based investors.

Crude Oil Resolution

The Strait of Hormuz tensions and US-Iran conflict are the primary reason crude is elevated. A de-escalation or agreement that reduces supply risk premium from oil prices would simultaneously improve India’s current account, support the rupee, and remove one of the key headwinds for domestic earnings. Watch the Middle East closely.

India Earnings Recovery

FPIs are not permanently allergic to India. They are disappointed in the earnings trajectory relative to valuations. If Q1 FY2027 earnings (April-June 2026) begin to show recovery, particularly in IT services (recovering US enterprise tech spending), banking (credit growth normalising), and consumer (rural demand recovery), the narrative can shift quickly. A resolution of the US-India trade negotiations would also unlock export-oriented sector confidence.

US Federal Reserve Rate Direction

If US inflation moderates enough for the Federal Reserve to begin cutting rates meaningfully, the yield differential between Indian and US bonds would improve, making India’s debt and equity markets more attractive on a relative basis. Fed rate cuts are a historical tailwind for emerging market inflows.

The China wildcard: A significant Chinese stimulus package or a major geopolitical resolution in Taiwan Strait tensions could cause a sharp rotation back into Asian emerging markets, including India. Conversely, an escalation of any of the active geopolitical conflicts (Middle East, South Asia) could extend the outflow cycle. Neither outcome is predictable in timing.

Final Thought

Rs. 2.25 lakh crore is an enormous number. But it is important to keep it in context. India’s total market capitalisation is approximately Rs. 400 lakh crore. The FPI outflow represents less than 0.6% of total market cap. What it represents in terms of sentiment and currency pressure is far larger than what it represents in terms of fundamental value destruction.

The long-term FPI story on India is not broken. India’s GDP growth remains 6-7% annually. The demographic dividend is intact. The formalisation of the economy continues. The digital infrastructure buildout continues. The PLI schemes are generating manufacturing investment. None of that has changed because FPIs sold Rs. 1.17 lakh crore in March.

What has changed is the short-term risk-reward calculation for dollar-based investors, driven by a combination of rupee weakness, oil prices, earnings disappointment, and better opportunities elsewhere. Those factors will eventually normalise. They always do.

For Indian retail investors, the FPI exodus of 2026 is not a reason to panic. It is a reason to understand what is driving valuations, to be selective about what they own, and to recognise that the domestic investor base is now large enough to prevent the extreme market dislocations that FPI selling used to produce.

The market is different now. The investor base is different. The SIP-powered DII presence means that large FPI exits create dips, not crashes. And dips, for the patient investor, are how long-term wealth is built.

GET IN TOUCH WITH US

For any query or personal assistance, feel free to reach out at support@altiusinvestech.com or call us at +91-6289225026.

Learn more about Unlisted Companies and Pre-IPO opportunities at Altius Investech.

Join our LinkedIn Newsletter: The Market Buzz by Altius