Two years ago, the EV two-wheeler story in India had one dominant narrative: Ola Electric was the category king, Ather Energy was the premium challenger, and the rest were noise. Today, Ather has listed and stabilised, Ola has lost half its market share and seen its stock crater 50% from its peak, and the market itself has been comprehensively reshuffled. TVS and Bajaj now lead. The unlisted opportunity has migrated to a new set of companies. This article maps exactly where things stand.

1. India’s EV Market: The Numbers That Matter

India’s EV two-wheeler market crossed 1.14 million units in FY2025, up 21% on FY2024’s 948,508 units, surpassing the million-unit milestone for the first time. That sounds impressive. But context matters: India sells roughly 17-18 million two-wheelers annually. EV penetration is still around 6-7%. The category is real and growing, but it is nowhere near the transition point that some of the early investor narratives implied.

The policy backdrop matters significantly. The government’s FAME II subsidy scheme provided critical demand support through FY2024. When FAME II subsidies were slashed in March 2025, the market braced for a sharp volume drop. Instead, OEMs responded with aggressive cash discounts, zero-cost EMI offers, and extended warranties, and April 2025 still registered record monthly sales. This resilience suggests that EV adoption in India has moved beyond pure subsidy dependency into genuine demand-pull territory.

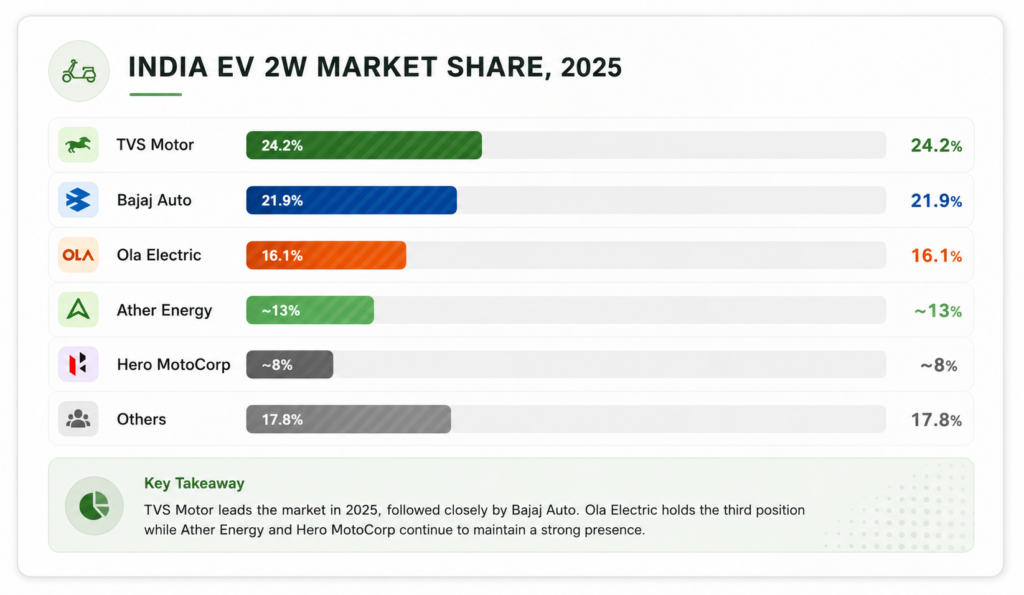

What has changed structurally is the competitive map. In FY2024, Ola Electric commanded 36.7% market share. By 2025, that share had collapsed to 16.1%. The gap was filled not by other EV startups but by legacy OEMs: TVS Motor, Bajaj Auto, and Hero MotoCorp with Vida. That shift has major implications for where the investable opportunity in India’s EV sector now sits.

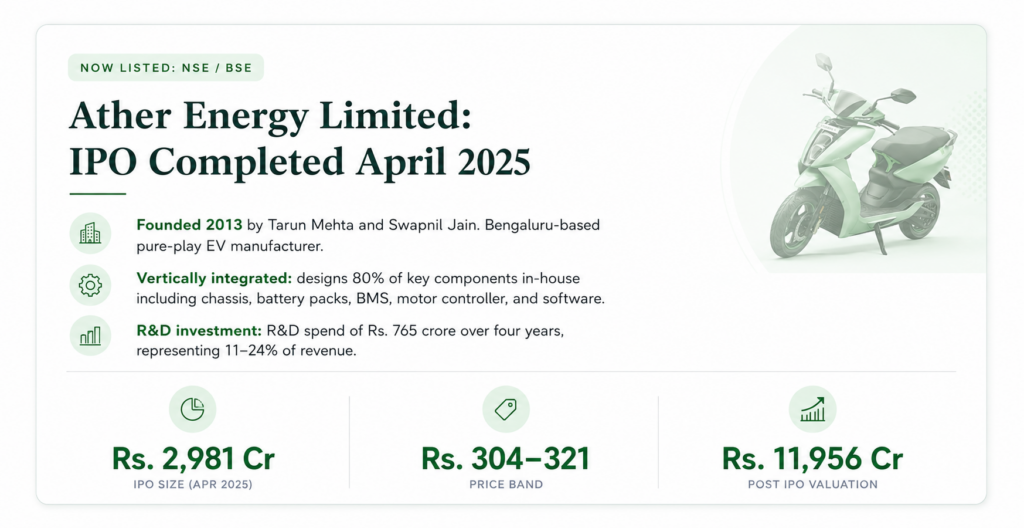

2. Ather Energy: From Unlisted Darling to Listed Reality

Ather Energy’s IPO in April 2025 was a significant moment for India’s EV sector. It was the second pure-play EV company to list after Ola Electric, and it arrived with markedly better investor perception despite trimmed valuations in the run-up to the listing.

The investment case for Ather is built on genuine differentiation. The company invested Rs. 765 crore in R&D over four years, representing 11-24% of revenue, far higher than the low-single-digit spending by traditional OEMs. It follows a vertically integrated model, designing 80% of key components in-house. Its IP portfolio includes 303 registered trademarks, 201 registered designs, and 45 registered patents as of February 2025, with many more applications pending.

What the Financials Show

For the nine months ending December 2024, Ather posted revenue of Rs. 1,578.90 crore, up from Rs. 1,230.40 crore in the same period a year ago. A net loss of Rs. 577.90 crore, significantly down from Rs. 776.40 crore a year earlier. The revenue from operations grew 329% between FY2022 and FY2024. Losses are narrowing even as revenue grows. The loss-to-revenue trajectory is moving in the right direction.

The company’s backer mix adds credibility: Hero MotoCorp holds approximately 30% post-IPO, providing industry depth, dealer network potential, and manufacturing credibility. GIC and NIIF trimmed stakes lightly at IPO but did not exit, signalling continued institutional confidence.

What the Pre-IPO Investors Got

For investors who accessed Ather through the unlisted secondary market in the 12-18 months before its IPO, the story played out as the unlisted thesis typically does. Pre-IPO prices for Ather shares on platforms like Altius Investech moved significantly as institutional interest in the upcoming listing grew. The IPO anchor book was fully subscribed, raising Rs. 1,340 crore from institutions before retail subscriptions even opened. Investors who got in through the unlisted route at earlier prices captured a meaningful portion of that premium before the general public had any access.

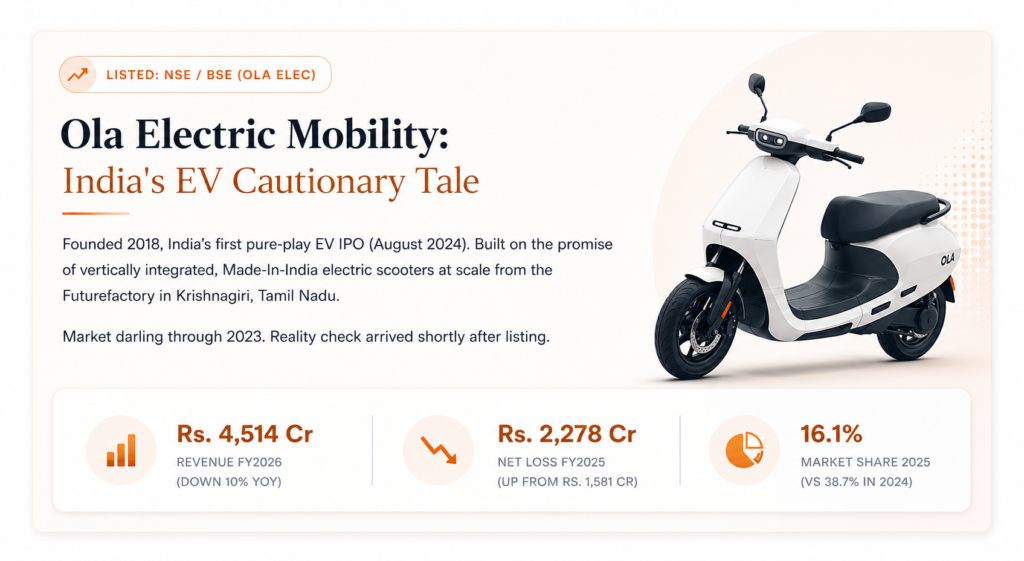

3. Ola Electric: The Rise, the IPO, and the Sharp Fall

Ola Electric’s story is the most instructive case study in what separates a great EV growth narrative from a great EV business. The company captured India’s imagination with its Futurefactory, its bold pricing, and its founder Bhavish Aggarwal’s relentless public presence. Its IPO in August 2024 was oversubscribed. The stock listed with enthusiasm.

Then reality arrived.

Ola Electric’s market position declined from 36.7% in 2024 to just 16.1% in 2025. Annual sales totalled 1,96,767 units in 2025, despite robust growth across the broader segment. The company’s share price dropped over 50% from its 52-week high. For FY2025, consolidated revenue stood at Rs. 4,514 crore, a 10% decline from the previous year. Net losses surged to Rs. 2,276 crore, up from Rs. 1,584 crore in FY2024.

What Went Wrong

The issues were operational, not technological. Customers reported ongoing problems with service response times and delivery reliability. Regulatory action in Goa suspended VAHAN registration for Ola scooters, blocking new sales in the state. The service network, a critical weakness from day one, became a mounting liability as volumes scaled and complaints accumulated.

Meanwhile, legacy OEMs fought back harder than Ola’s planning had assumed. TVS’s iQube and Bajaj’s Chetak offered something Ola could not: decades of dealer network trust and after-sales infrastructure that urban buyers, especially outside metro areas, valued more than feature lists.

The Ola lesson for EV investors: In the Indian two-wheeler market, first-mover advantage in product is meaningless without service network depth. Ola Electric built a great factory and a distinctive scooter. It did not build the post-purchase experience that retains customers and drives word-of-mouth in a category where Rs. 1-1.5 lakh is a significant household purchase decision. That gap has proved far more damaging than any technology shortcoming.

The company is not done. Ola’s Roadster X electric motorcycle, launched in early 2026, represents a genuine product pivot toward a higher-margin, lower-service-intensity category. And the auto business did report a slim positive EBITDA margin of 0.3% in Q2 FY2026, suggesting the manufacturing economics are improving even as volumes drop. Whether Ola can rebuild customer trust is the central question for the next two years.

4. The Incumbents Strike Back: TVS, Bajaj, and Hero

The most important development in India’s EV two-wheeler market in 2025 was not anything a startup did. It was the systematic rise of the incumbents.

TVS Motor claimed the top position in 2025 with a 24.2% market share, registering sales of 2,95,315 units. Bajaj Auto secured second place with 21.9% of the market. Hero MotoCorp’s Vida registered 540% year-on-year growth in April 2025 alone.

This reshuffling has a clear implication for the listed equity story: the best way to own India’s EV transition through public markets is probably not through pure-play EV companies at all. It is through TVS Motor and Bajaj Auto, which have both diversified revenue bases (protecting downside) and accelerating EV market share (capturing upside). Both are already profitable, already listed, and already demonstrating that their decades of distribution infrastructure translate directly into EV adoption advantage.

5. Who Is Left in the Unlisted EV Space

With Ather and Ola Electric now listed, the unlisted EV opportunity has migrated. Here are the companies that remain in the pre-IPO space and are worth tracking in 2026.

Performance Electric Motorcycles

Ultraviolette Automotive

Bengaluru-based manufacturer of the F77, celebrated as India’s first performance-oriented electric motorcycle. Raised $45 million in total funding. Manufacturing capacity of 10,000 units annually, scalable to 30,000. Debuted at EICMA 2024 in France, signalling global ambitions. Launched the X47 crossover in October 2025. Backed by TVS Motor Company and other institutional investors.

Battery Swapping / Micro Mobility

Bounce Infinity

Operator of India’s first electric scooter with a swappable battery system. The Infinity E1 and E2 models target urban commuters and the gig economy. Battery-as-a-Service model lowers upfront ownership cost, addressing the single biggest barrier to EV adoption in the mass market. Actively expanding its swap station network across Tier 1 and Tier 2 cities.

Electric Three-Wheelers / Last Mile

Euler Motors

Focused on electric commercial three-wheelers for last-mile delivery. Counts Amazon, Zomato, and Swiggy among customers. A direct beneficiary of India’s booming e-commerce fulfilment demand. B2B model with more predictable revenue and clearer unit economics than consumer-facing EV companies.

Electric Charging Infrastructure

Exponent Energy

Building the infrastructure for ultra-fast EV charging, targeting 0-100% charge in 15 minutes for commercial vehicles. B2B focus on fleet operators and logistics companies. Raised significant VC funding. As EV penetration rises, charging infrastructure becomes as critical as the vehicles themselves, and potentially more defensible as a business.

Battery Technology / Cell Manufacturing

Battery Smart

India’s largest battery swapping network, with over 2,500 swap stations across the country. Backed by Tiger Global and others. Operates predominantly in the electric three-wheeler and rickshaw segment, which represents a large and underserved market. Asset-light model with network effects as density increases.

Electric Commercial Vehicles

Altigreen Propulsion Labs

Focused on electric three-wheelers for cargo and passenger transport. Targets fleet operators in urban last-mile logistics. Has partnerships with major logistics companies and raised institutional funding for manufacturing scale-up. A lower-profile name relative to consumer two-wheeler brands but with cleaner unit economics.

Where the real unlisted opportunity sits in 2026: The most interesting unlisted EV companies are no longer in consumer two-wheelers (the Ola-Ather category). They are in adjacent infrastructure: battery swapping networks, ultra-fast charging, electric commercial vehicles, and component technology. These businesses have lower consumer brand visibility but stronger B2B revenue models, clearer paths to profitability, and less exposure to the consumer sentiment swings that have hurt Ola Electric.

6. The Investor Framework for EV in 2026

| Category | Opportunity Type | Risk Level | Best Access Route |

|---|---|---|---|

| TVS Motor, Bajaj Auto | EV market share + diversified ICE base | Low-Medium | Listed market (NSE/BSE) |

| Ather Energy | Pure-play premium EV, post-IPO | Medium | Listed market (NSE/BSE) |

| Ola Electric | Recovery play, high uncertainty | High | Listed market (NSE/BSE) |

| Ultraviolette | Performance segment, global ambition | Medium-High | Unlisted secondary market |

| Battery Smart / Bounce Infinity | Infrastructure play, network effects | Medium-High | Unlisted secondary market |

| Euler Motors / Altigreen | B2B commercial EV, cleaner economics | Medium | Unlisted secondary market |

| Exponent Energy | Charging infrastructure, fleet focus | Medium-High | Unlisted secondary market |

Final Thought

India’s EV revolution is real. The numbers confirm it. Over a million electric two-wheelers sold in a single year, with a government target of 80% EV penetration in two-wheelers by 2030, and a domestic manufacturing base that is rapidly building depth in batteries, motors, and electronics. The structural case has not changed.

What has changed is who benefits from it. The Ola Electric experience demonstrated that narrative-driven valuations at IPO do not automatically translate into post-listing returns. Ather’s more measured IPO, with genuine technology depth and improving financials, has fared considerably better.

For investors approaching this sector today, the most interesting risk-adjusted positions may not be in the two-wheeler consumer brands at all. They are in the infrastructure layer of India’s EV ecosystem: the charging networks, the battery swapping platforms, the commercial vehicle electrification plays. These businesses are less visible, less exciting at a dinner party, and far less likely to be the subject of breathless startup journalism. They are also far more likely to be structurally profitable at scale.

The EV revolution will happen. The question, as always in investing, is not whether the theme is right. It is which companies capture its value. And in India’s EV sector in 2026, that answer looks quite different from what most people would have predicted in 2022.

GET IN TOUCH WITH US

For any query or personal assistance, feel free to reach out at support@altiusinvestech.com or call us at +91-6289225026.

Learn more about Unlisted Companies and Pre-IPO opportunities at Altius Investech.

Join our LinkedIn Newsletter: The Market Buzz by Altius