Every plastic bottle you throw away ends up somewhere. In India, a growing number of them end up at the gates of a factory in Kashipur, Uttarakhand, where they are shredded, washed, melted, and spun into what the industry calls “Green Fibre.” The company doing it is Pashupati Polytex, and most investors have never heard of it. That gap between visibility and value is exactly where unlisted market opportunities are found.

1. What Pashupati Polytex Actually Does

Most people understand recycling in a vague, ambient sense. You put a bottle in the blue bin. Something good happens. Pashupati Polytex is a significant part of that “something good” in India.

The company collects post-consumer PET (polyethylene terephthalate) bottles, the plastic used in virtually every water bottle, soft drink bottle, and cooking oil container in the country. These bottles go through a multi-stage industrial process: sorting, baling, shredding into flakes (rPET flakes), washing, drying, melting, and extrusion into fibre form. The output is Recycled Polyester Staple Fibre (rPSF), also called “Green Fibre,” which is sold to textile mills that use it to make yarn, fabric, and a range of end products including cushioning, carpets, non-woven fabrics, and geotextiles.

It is not a glamorous business by any measure. But it is an essential one. And in a country that generates 9.4 million tonnes of plastic waste annually, with new Extended Producer Responsibility (EPR) regulations compelling brands to recycle a percentage of their plastic packaging, Pashupati Polytex is sitting at the convergence of industrial necessity and regulatory mandate.

2. The Pashupati Group: A Family Enterprise Built Around Recycling

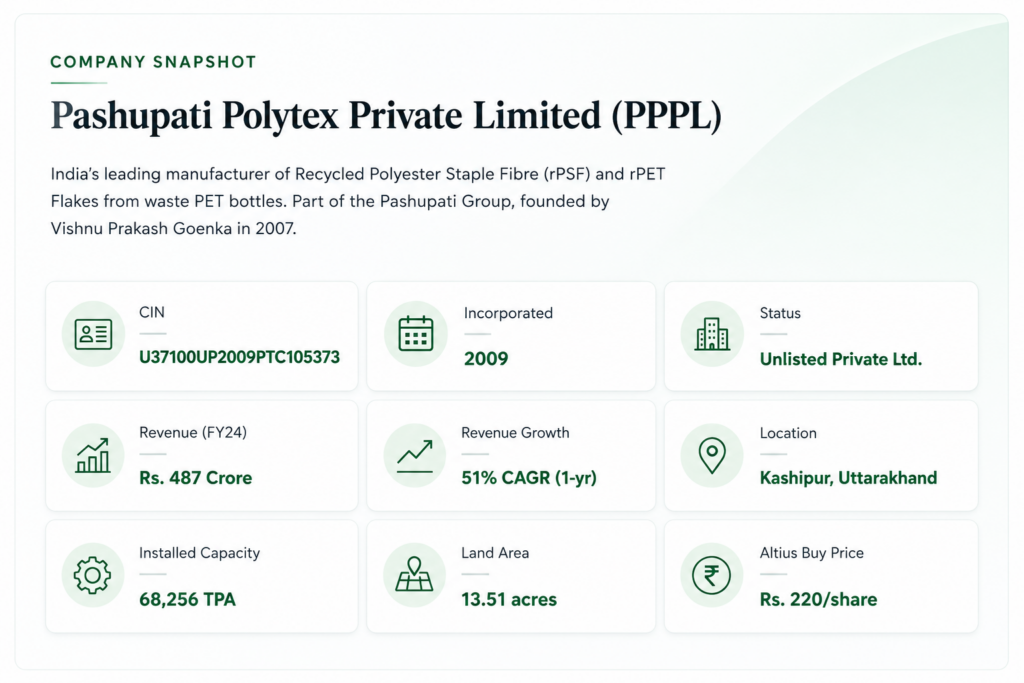

Pashupati Polytex does not exist in isolation. It is the flagship manufacturing entity of the Pashupati Group, a recycling-focused industrial conglomerate founded by Vishnu Prakash Goenka in Gorakhpur, Uttar Pradesh, in 2007.

The group’s timeline is a story of systematic vertical integration. It began with Pashupati Laminators in 2007, manufacturing woven fabrics and PP woven bags. In 2009, Pashupati Polytex was incorporated to manufacture rPSF. By 2016, the group had added Pashupati Extrusions for PET chips manufacturing. In 2018, it launched Kundana TechnoTex to serve South India and export markets. By 2022, additional units at Kundana, Salasar, and Saurabh Clean Tech were commissioned.

Today, the Pashupati Group operates eight manufacturing plants across India, with concentrations in Kashipur (Uttarakhand) and Jaipur (Rajasthan), and has raised $36 million in institutional funding. The group employs approximately 363 people and is growing headcount at 15% year on year.

The founder and CMD, Vishnu Prakash Goenka, brings 45 years of industrial experience. His son Bankey Bihari Goenka serves as Managing Director and handles day-to-day operations. This is a family-led enterprise with deep operational roots, not a promoter-backed shell running a listing-driven narrative.

3. Products: Beyond Basic Recycling

The most important thing to understand about Pashupati Polytex’s competitive positioning is that it does not just make commodity rPSF. It manufactures a sophisticated and growing range of specialty fibres that command significantly higher margins than basic recycled fibre.

Its R&D division has developed and commercialised the following product lines:

- Solid rPSF and Hollow rPSF: Standard recycled fibre used in textile yarns, cushioning, and stuffing applications.

- P-Concrett (Reinforcement Fibre): rPSF specifically engineered for concrete reinforcement in construction applications. Branded and marketed as a speciality product.

- P-Anti Bacterial: Fibre with antimicrobial properties for hygiene-sensitive textile applications.

- P-Acro Fill (Hydrophilic Fibre): Moisture-wicking fibre for sportswear, medical textiles, and filtration applications.

- Fire Retardant Fibre: For safety-critical applications including automotive interiors, public transport seating, and protective clothing.

- Biodegradable Fibre: An emerging product line targeting sustainable packaging and textile applications.

- rPET Flakes and rPET Chips: Used directly by PET processors, bottle manufacturers, and food-grade packaging producers.

- Recycled Synthetic Yarns: Downstream integration into yarn manufacturing, adding further value to the recycling chain.

The specialty fibre portfolio is significant for one reason: it is not commoditised. A buyer cannot simply switch suppliers for P-Concrett or Fire Retardant rPSF the way they can for generic recycled polyester. This creates pricing power, customer stickiness, and margins that commodity producers cannot access.

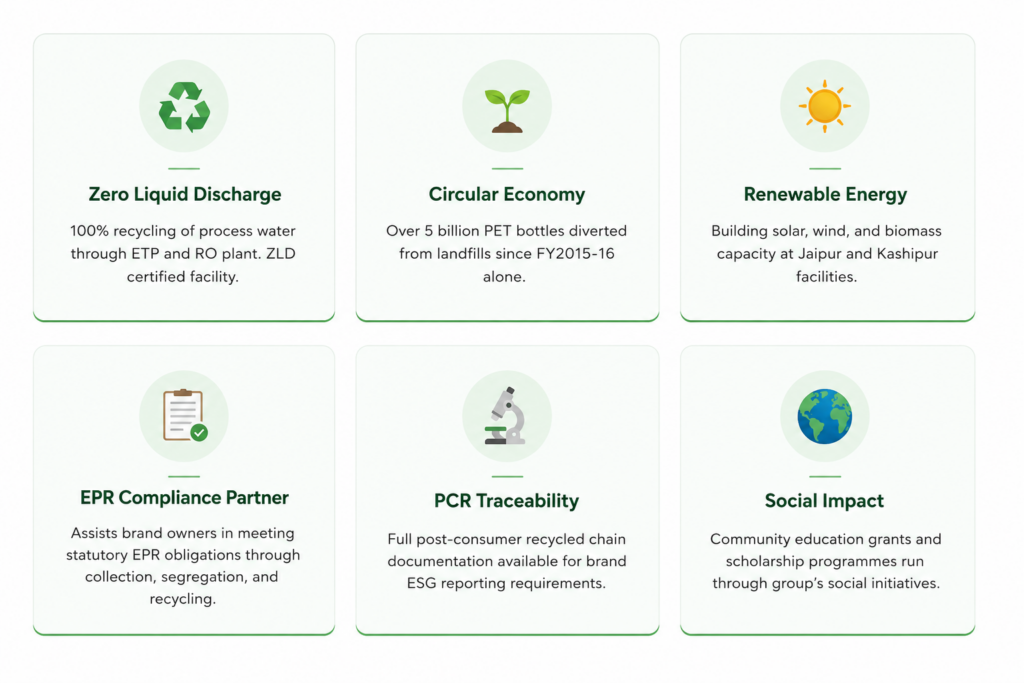

Traceability as a competitive moat: Pashupati Polytex has built its own waste management vertical, giving it direct control over raw material sourcing: waste PET bottles. This “Post-Consumer Recycled” (PCR) chain with full traceability is becoming increasingly important as brand owners (FMCG companies, fashion brands, sportswear companies) need to verify and certify the recycled content in their supply chains for ESG reporting. Pashupati can provide that documentation. Most competitors cannot.

4. Financials: The Numbers That Matter

Pashupati Polytex is a private company, which means detailed financial disclosures are limited. However, based on regulatory filings and publicly available information, here is what investors can work with.

| Metric | FY2024 | FY2025 (Group est.) | Notes |

|---|---|---|---|

| Revenue (PPPL) | Rs. 487 Crore | N/A (standalone) | 51% YoY growth in FY24 |

| Group Revenue | N/A | Rs. 591 Crore | All group entities combined |

| Authorised Share Capital | Rs. 64.35 Crore | Rs. 64.35 Crore | MCA filings |

| Paid-Up Capital | Rs. 50.28 Crore | Rs. 50.28 Crore | MCA filings |

| Employee Count (Group) | ~315 | ~363 (+15% YoY) | Tracxn data Jan 2025 |

| Total Funding Raised | $36 million | $36 million | Across 1 institutional round |

| Unlisted Share Price (Altius) | N/A | Rs. 220 per share | As of May 2026, subject to market conditions |

The headline number is the revenue growth. 51% year-on-year growth in FY2024 is not a number that most manufacturing companies post at this scale. It signals that either capacity utilisation is ramping sharply, pricing has improved materially, new product lines are gaining traction, or some combination of all three. In the absence of detailed audited P&L disclosures, investors should seek these clarifications directly before taking a position.

Important context on share price: Pashupati Polytex’s unlisted price of Rs. 220 per share is based on demand-supply dynamics in the unlisted market, comparative peer valuations of listed rPSF and plastic recycling companies, and the most recent funding round benchmarks. This is not a SEBI-regulated quoted price. It is an over-the-counter market price and can move materially based on market sentiment and transaction volume.

5. The ESG Angle: Why This Matters More Than Ever

In 2022, SEBI introduced the Business Responsibility and Sustainability Report (BRSR) framework, mandating ESG disclosure for listed companies above a certain size. More significantly, India’s Extended Producer Responsibility (EPR) rules under the Plastic Waste Management Rules now require brand owners and importers to take back, recycle, or co-process the plastic they put into the market.

This regulatory architecture is a structural tailwind for Pashupati Polytex. Every FMCG company with a plastic packaging footprint now needs a certified recycling partner. Every apparel brand seeking to incorporate recycled polyester into its supply chain needs a traceable source of rPSF. Pashupati Polytex provides both.

The strategic value of this ESG positioning cannot be overstated. Global fashion brands, packaged goods companies, and sportswear manufacturers are under intense pressure from investors and consumers to demonstrate sustainable sourcing. Recycled polyester fibre with verified PCR content and full traceability commands a premium price. Pashupati Polytex’s integrated waste management vertical gives it that credential in a way that most competitors in the Indian market cannot replicate.

6. Market Opportunity: India’s Plastic Recycling Mandate

India generates approximately 9.4 million tonnes of plastic waste per year, according to the Central Pollution Control Board. Of this, PET plastic (the type Pashupati Polytex processes) accounts for a significant and growing share, driven by the explosion of packaged beverages, personal care products, and food packaging in India’s expanding consumer market.

The government’s policy direction is unambiguous. The Plastic Waste Management Rules 2016, amended substantially in 2022, mandate phase-outs of single-use plastics and impose EPR obligations on producers. The National Policy on Biofuels and various state-level Green Credit Programme initiatives add further incentives for plastic collection and processing companies.

India’s recycled polyester fibre market is currently valued at approximately Rs. 8,000-10,000 crore and is growing at over 15% annually, driven by:

- Mandatory EPR compliance creating structural demand for certified recyclers

- Global textile brands shifting to recycled content in their supply chains

- India’s growing sportswear, athleisure, and technical textile markets

- Construction sector adoption of rPSF in concrete reinforcement

- Government infrastructure programmes increasing demand for geotextile applications

Pashupati Polytex has an installed capacity of 68,256 TPA. At full utilisation, this represents a significant share of India’s organised rPSF manufacturing capacity. The company has been expanding steadily since its founding in 2009, when it started with just 1,200 TPA.

7. Risks Investors Should Know

Pashupati Polytex is an interesting unlisted opportunity, but it is not without material risks. Investors should weigh the following before taking a position.

Raw Material Price Volatility

rPSF production economics are tightly linked to PET bottle availability and price, crude oil-derived virgin polyester prices (which compete with recycled fibre), and freight costs for waste collection. Any disruption in PET waste supply chains or a sharp drop in virgin polyester prices (which reduces the premium that recycled fibre commands) can compress margins significantly.

Commodity Pricing Pressure

Despite the specialty fibre portfolio, the majority of revenue likely still comes from standard-grade rPSF, which is a commodity. When capacity in the industry exceeds demand, pricing falls. India’s recycling capacity has been expanding rapidly, and competitive pressure from other rPSF manufacturers including Reliance Industries’ recycling initiatives is real.

No IPO Clarity

Unlike Zepto or Niva Bupa, Pashupati Polytex has no publicly stated IPO timeline. This means liquidity in the unlisted market is the primary exit mechanism for investors. The unlisted share market in India has grown significantly, but it remains less liquid than public markets. Investors should factor in a 3-5 year holding horizon with no guaranteed exit.

Family-Owned Management Concentration

The Pashupati Group is tightly controlled by the Goenka family. Governance structures in family-owned private companies can differ from publicly listed entities. Limited external audit visibility, fewer independent directors, and concentrated decision-making authority are all factors to assess before investing.

Limited Financial Disclosure

As a private limited company, Pashupati Polytex is not required to file detailed quarterly results or maintain the disclosure standards of a listed company. Investors work with annual filings, which are typically 9-12 months old by the time they are publicly accessible. This information asymmetry is a feature of the unlisted market, not a bug exclusive to this company, but it requires greater due diligence.

Bottom line on risk: Pashupati Polytex is a real business with real revenue, a credible sustainability moat, and a growing market behind it. It is not a pre-revenue startup. But it is also not a company with the governance transparency of a listed entity. Invest with an appropriate position size and a multi-year horizon.

8. The Investor Verdict

Why Pashupati Polytex Is Interesting

- 51% revenue growth in FY2024 signals rapid scale-up

- Diversified specialty fibre portfolio creates pricing power beyond commodity rPSF

- Full vertical integration from waste collection to fibre output is a defensible moat

- EPR mandates create structural, regulatory-backed demand for certified recyclers

- ESG credentials align perfectly with global supply chain sustainability requirements

- ZLD status and traceability infrastructure ahead of industry peers

- Rs. 220 per share entry point with Rs. 50.28 crore paid-up capital gives a relatively accessible investment threshold

- Broader Pashupati Group revenue of Rs. 591 crore adds group-level robustness

Why Investors Should Be Cautious

- No IPO timeline or listing event confirmed

- Limited financial disclosure makes deep analysis difficult

- Commodity pricing risk in standard-grade rPSF

- Competition from Reliance and other large-capacity players expanding into recycled fibre

- Family-owned governance structure with limited external oversight

- Unlisted market liquidity is thin; exit depends on finding a counterparty

- Raw material (PET waste) availability and pricing add margin volatility

Pashupati Polytex occupies a rare and valuable niche: it is a high-growth manufacturing business with genuine ESG credentials in a market that is being structurally expanded by regulatory mandate. That combination is not common in India’s unlisted space, which tends to attract either capital-light tech businesses or commodity manufacturers without differentiation.

The company’s growth rate, capacity footprint, and specialty product portfolio make it worth serious consideration for investors comfortable with the illiquidity and governance characteristics of the unlisted market. It is not a short-term trade. It is a bet on India’s plastic recycling infrastructure becoming more, not less, economically valuable over the next five years.

That bet has a solid regulatory and environmental thesis behind it. Whether the timing and price are right is a question each investor must answer for themselves.

GET IN TOUCH WITH US

For any query or personal assistance, feel free to reach out at support@altiusinvestech.com or call us at +91-6289225026.

Learn more about Unlisted Companies and Pre-IPO opportunities at Altius Investech.

Join our LinkedIn Newsletter: The Market Buzz by Altius