OYO Rooms is one of the most dramatic entrepreneurial stories to emerge from India — a company that went from a teenager’s ₹1 crore seed to a $10 billion global giant, then imploded, then quietly rebuilt itself from rubble into profitability. Today, as it approaches a long-anticipated IPO, its unlisted share price sits at ₹27.

Understanding why that price is where it is requires understanding the full arc of OYO’s history: every reckless bet, every brilliant pivot, and every lesson in what venture capital does to a promising idea when there are no guardrails.

1. The 2013 Founding: A Teenager Who Said No to College

Ritesh Agarwal and the Thiel Fellowship

In 2012, a 17-year-old from the small town of Bissam Cuttack in Odisha arrived in Delhi with two things: a knack for coding and a visceral frustration with India’s budget accommodation market.

Ritesh Agarwal had been travelling cheaply across the country, staying in dingy guest houses that had no consistency — you never knew whether the room would have clean linen, a working AC, or even hot water.

He built Oravel Stays, a website that let small properties list their rooms — essentially an Airbnb clone. It did not catch on. But the idea of fixing India’s fragmented, untrusted budget hospitality sector was the right one.

In 2013, Agarwal applied for the Thiel Fellowship — a $100,000 grant from Peter Thiel’s foundation for entrepreneurs under 23 to skip college and build companies. He became the first Asian resident ever selected.

What OYO Actually Did Differently

The pivot from Oravel to OYO (On Your Own) was product-market fit in action. Instead of listing existing rooms as-is, OYO would franchise them under a standardised brand.

Every OYO-branded room would guarantee a minimum set of amenities:

- Clean, ironed linen changed at every checkout

- Functional air conditioning

- Free Wi-Fi and a 32-inch television

- A clean, attached washroom

Property owners would pay OYO a commission on bookings in exchange for branding, technology, and demand generation.

Guests would book via OYO’s app and get a consistent experience — no surprises.

OYO would never own the rooms. Zero capex. Pure asset-light franchise play.

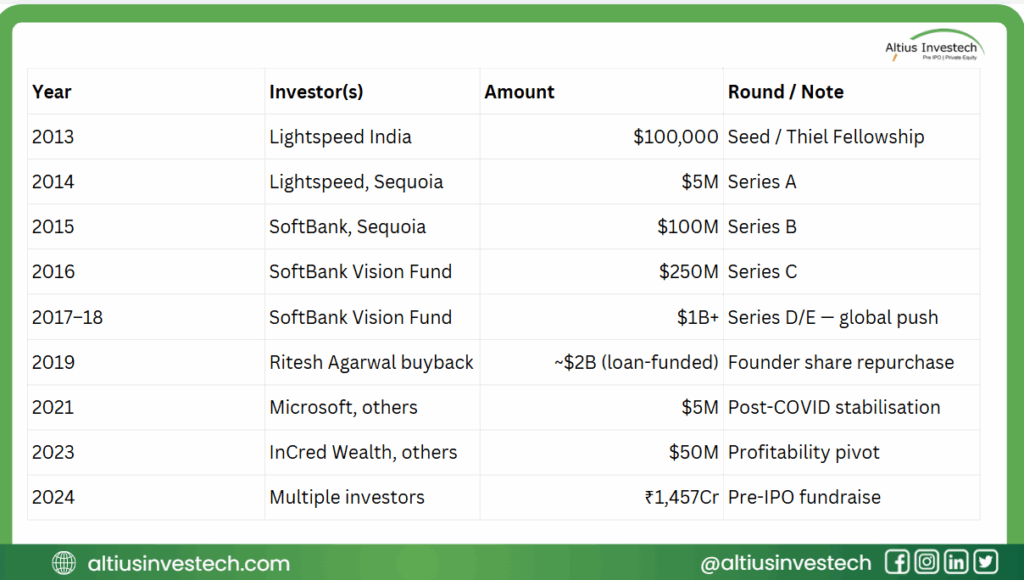

The first OYO hotel launched in Gurugram in 2013. By 2016, OYO had crossed 50,000 rooms and raised $100 million from SoftBank. Agarwal was 22 years old.

Why the Model Made Sense for India

India had — and has — millions of small, independent hotels and lodges that are structurally incapable of building a brand or attracting online bookings on their own.

OYO gave them:

- Distribution

- Technology

- A recognisable brand

For travellers, it solved a genuine trust deficit.

The model was simple, scalable, and uniquely suited to a fragmented hospitality market. These fundamentals were sound — and they remain sound today.

2. The SoftBank Era

Funding Timeline and Capital Raised

OYO’s fundraising history reads like a parable about what happens when capital becomes cheap and speed becomes the only metric.

The $10 Billion Peak

Between 2017 and 2019, OYO transformed from an Indian budget hotel aggregator into a sprawling global conglomerate.

At peak expansion:

- 800+ cities across 80+ countries

- 850,000 rooms globally

- 23,000 hotel properties

- 12,000 employees

SoftBank’s Vision Fund turned OYO into one of its marquee bets.

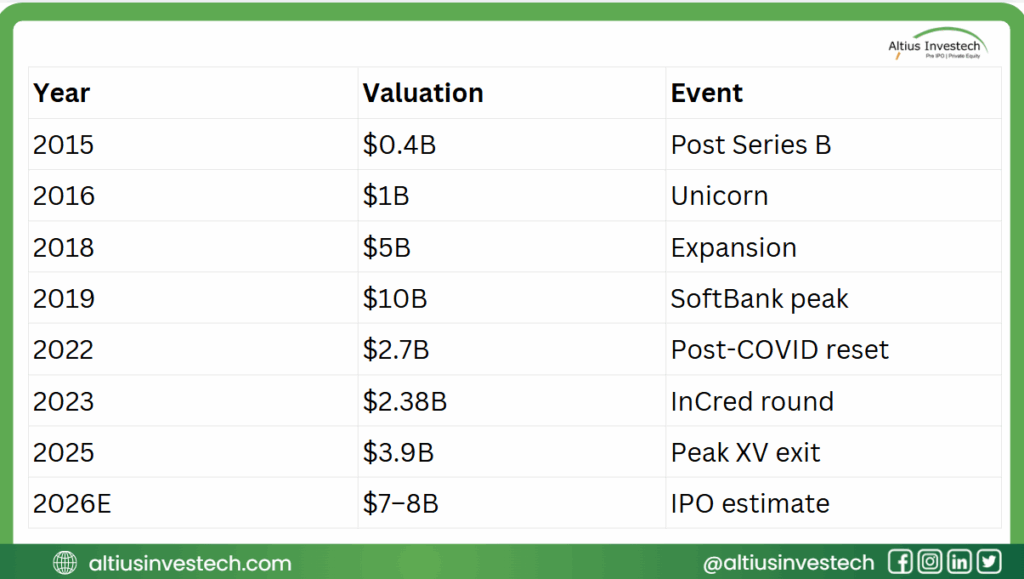

The valuation peaked at $10 billion in 2019.

The Founder Buyback — A Bet Within a Bet

In 2019, Agarwal borrowed approximately $2 billion from Japanese banks, collateralised against his OYO shares.

He used the money to buy back stakes from early investors including Lightspeed and Sequoia.

His ownership jumped from ~9% to ~33%.

If OYO succeeded — the move was genius.

If it failed — the consequences would be severe.

Where the Model Started Breaking

Several structural problems emerged.

Lease model risk

OYO began signing master lease agreements, paying fixed rent for entire buildings.

When occupancy dropped, losses ballooned.

By 2019 OYO had accumulated ₹3,000+ crore in lease obligations.

China disaster

OYO attempted to out-execute Chinese hospitality giants like Huazhu and Meituan.

It reportedly signed 10,000+ properties in under 18 months, many of which were fraudulent listings.

Partner revolt

Hotel partners complained about:

- unpaid dues

- overbooking

- technology failures

Unit economics collapse

OYO was burning ₹5,000+ crore per year in FY2020.

The company had confused growth with health.

They are not the same thing.

3. The Crash: $10 Billion to $2.7 Billion

COVID-19 as Accelerant, Not Cause

When the pandemic hit in 2020, global travel collapsed.

For OYO, this merely exposed deeper structural issues.

Consequences included:

- 5,000 layoffs globally

- massive market exits

- partner disputes

- valuation crash

Valuation fell from $10B → $2.7B (73% drop).

Valuation Timeline

4. The Comeback: How OYO Turned Profitable

Beginning in late 2020, OYO underwent a major restructuring.

Key strategic changes

- Exit asset-heavy lease model

- Reduce headcount 12,000 → 3,500

- Focus on India + Europe vacation rentals

- Launch OYO OS property management platform

- Restructure debt

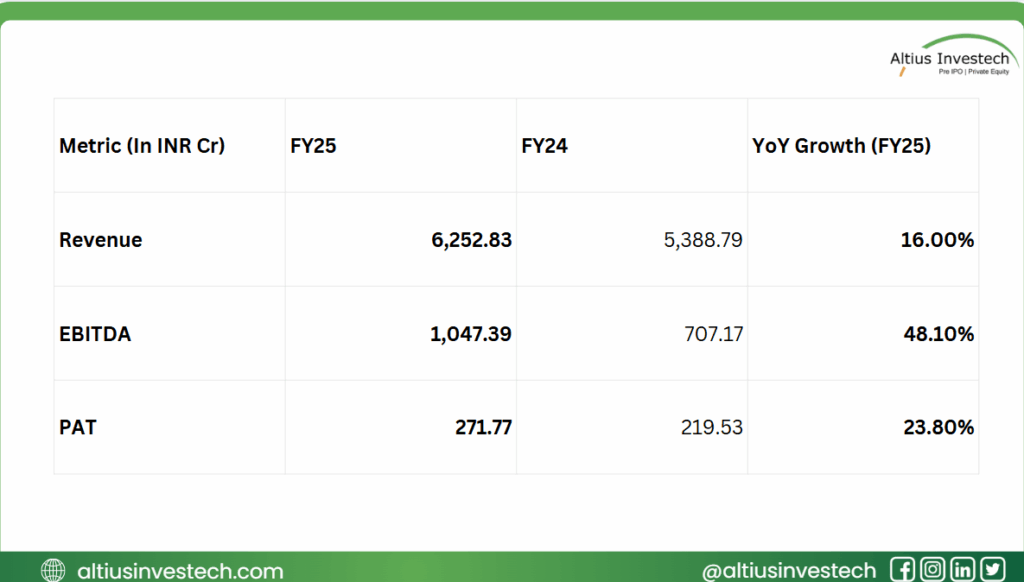

Financial Performance

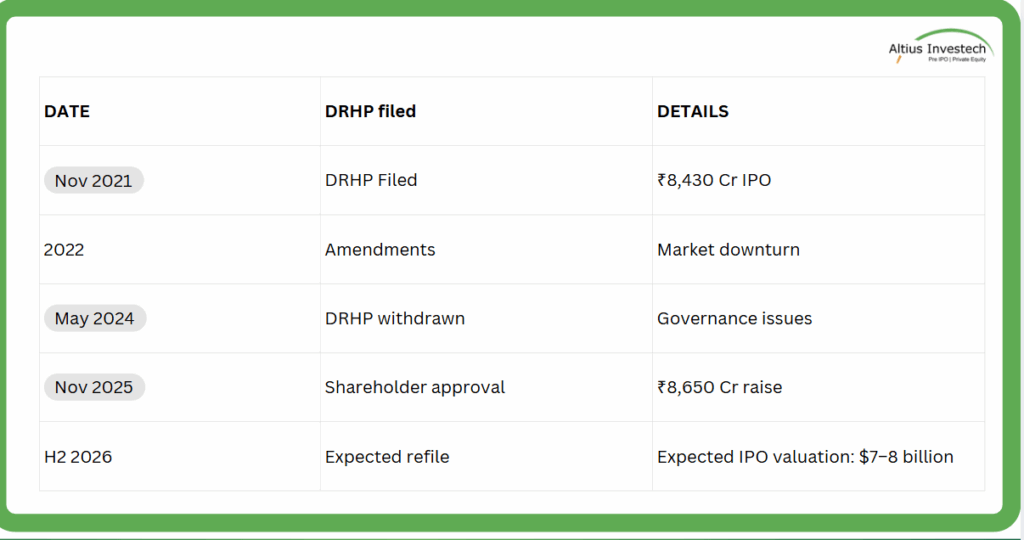

5. The IPO Timeline: A Story of False Starts

6. Valuation Snapshot: IPO vs Current Unlisted Market

Based on latest available data (FY25), OYO (PRISM / Oravel Stays) is currently valued at a market capitalisation of ~₹37,800 crore, translating to a price of ~₹27 per share on the Altius platform.

Key valuation metrics (FY25):

- Market Cap: ~₹39,079 Cr (Approx)

- Price per Share: ~₹26.5

- P/E: ~147.22x

In comparison, the confidential IPO filing targets a valuation of USD 7–8 billion, equivalent to approximately ₹58,000–66,500 crore. This implies a meaningful valuation gap between current unlisted pricing and the potential IPO range.

What this indicates:

- The market is currently valuing OYO at a discount to its likely IPO valuation, despite improved profitability and operating leverage.

- At ~₹27 per share, current pricing reflects conservative expectations, whereas the IPO range prices in future growth, premiumisation, and global scale.

- If the IPO is executed closer to the indicated range, it could offer valuation re-rating potential for existing unlisted shareholders.

Bottom line: The valuation snapshot highlights a clear divergence between current secondary-market pricing on Altius and expected IPO valuation, making this phase particularly relevant for investors tracking OYO’s public-market transition.

Conclusion

OYO’s story is not simply success or failure.

It is a survival story.

A visionary start.

A reckless expansion.

A brutal crash.

And a quiet, disciplined turnaround.

Whether ₹27 represents a bargain or a warning depends on how patient investors are willing to be.

The hotel is open for business.

The only question is when investors check ou

Looking to invest in more high-potential companies like OYO?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of February 24th, 2026, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)