A persistent, often heated debate dominates the dinner tables of India’s rising middle class: Where does capital actually compound the most efficiently over a long-term horizon?

Since the global financial crisis of 2008, the Indian equity market has been one of the most consistent wealth-creation engines on the planet. With Demat accounts surging past the 21 crore mark, the conversation among retail investors has finally matured. It is no longer just about “saving” money; it is about optimal capital allocation.

For decades, the standard playbook offered a binary choice: the structured safety of Mutual Funds or the active pursuit of alpha through Direct Stocks. However, as the landscape of pre ipo investing has democratised, unlisted shares have crashed the party. They bring a completely different risk-reward profile, one that used to be the private playground of billionaires.

🌱 The Foundation — Why Mutual Funds Are the Starting Point, Not the Destination

Any objective financial analysis must begin with the baseline: the public index. Mutual funds are the absolute anchor of domestic wealth creation. They offer instant diversification, rigorous regulatory safety via SEBI, and professional, emotionless management.

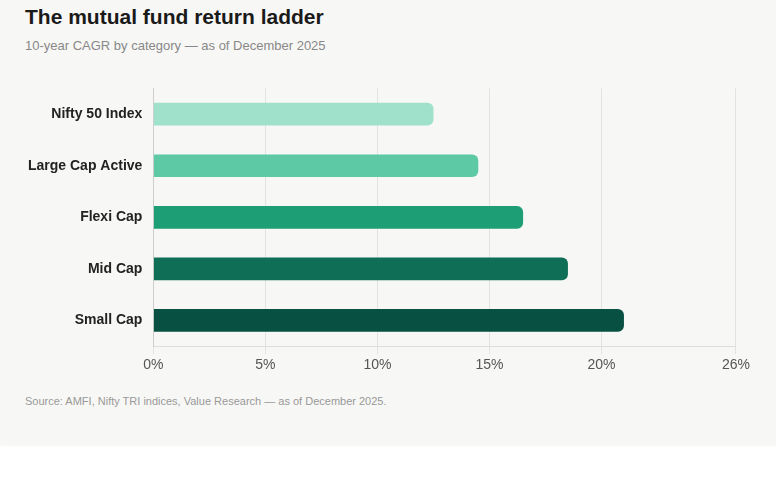

If you had taken ₹10 Lakhs and passively parked it into a standard Nifty 50 index fund 10 years ago, you would have captured a Compound Annual Growth Rate (CAGR) of roughly 12% to 13%.

Let’s look at what that actually means:

Actively managed funds have pushed those baseline averages even higher. Well-regarded large and flexi-cap funds historically hover in the 14% to 16% annualized range. If you were willing to stomach more volatility and allocate capital to top-tier small-cap funds, the 10-year historical averages often sit between 18% and 22%.

At a 20% annualized return, wealth compounds aggressively. Mutual funds are, undeniably, the most reliable vehicle for long-term financial security.

🧾 The Catch: The “Maturity Tax”

Mutual funds buy maturity, not momentum. By the time a company enters a large fund portfolio, the 10x journey from ₹500 crore to ₹5,000 crore is already history. You are paying for stability — and sacrificing the multiples that came before it.

🎯 The Alpha Hunt — Navigating the Volatility of Listed Stocks

Direct equity investing is the natural progression for the investor looking to beat that 15% mutual fund average. If an investor had the deep conviction to buy legacy consumer or financial stocks 15 years ago and the iron stomach to hold them through multiple market cycles, they generated massive, generational wealth.

But analysing direct stocks requires a harsh reality check.

Statistically, the average retail investor consistently fails to beat the benchmark index over 15 years. Why? Because of the Behavioural Tax.

- Panic Selling: Retail investors often liquidate during 30% market corrections.

- Performance Chasing: Buying at the top of a hype cycle and selling at the bottom.

- Poor Selection: Holding onto losing stocks out of hope while selling winners too early.

Furthermore, when buying a listed stock, you are paying a valuation that has been heavily vetted, priced, and marked up by sophisticated investment bankers during its IPO. Because the stock is liquid, meaning you can sell it in milliseconds on your phone, you are paying a premium for that exact convenience. You are paying for public liquidity.

🔔Before the Bell Rings — The Case for Owning Companies Before They Go Public

This brings our analysis to the unlisted market, the core focus of our thesis at Altius Investech.

It is a common analytical mistake to compare the average mutual fund return against the single best outlier in pre ipo shares. Unlisted markets carry unique risks, your capital is locked in, and the journey to an IPO is rarely a straight line.

However, when examining broad institutional data, the average targeted Internal Rate of Return (IRR) for a well-constructed pre-IPO portfolio typically ranges from 20% to 25%, representing a substantial premium over public markets.

At Altius, we emphasise that this higher average is not driven by magic, luck, or speculative gambling. It is driven by two fundamental financial mechanics that the smartest money in the room has exploited for decades:

- The Illiquidity Premium: Because you cannot liquidate unlisted equity shares with a simple swipe on your phone, the market rewards you with a heavily discounted entry price. You are being paid a premium for your patience.

- Valuation Arbitrage: Capital in the unlisted space is deployed during a company’s most aggressive scaling phase. You are capturing the massive gap between what a private business is structurally worth (based on its cash flows) and the premium “hype” multiple the retail public is willing to pay on listing day.

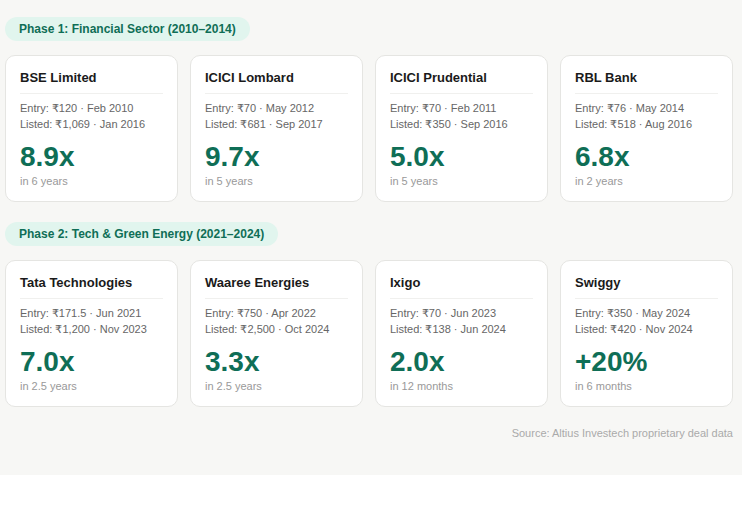

💰 The Track Record

When this investment thesis is executed correctly, the individual case studies from the last 15 years show exactly how these returns pull a portfolio’s overall average to staggering heights. We track these historical data points closely across every market cycle:

👉 See all past deals returns:https://altiusinvestech.com/about

⚖️Rethinking Capital Allocation

When evaluating Unlisted Shares vs. Mutual Funds vs. Direct Equities, the Altius view is that there is no single “correct” asset class, only the correct tool for specific financial goals.

If a portion of your portfolio requires absolute liquidity, regulatory comfort, and a steady 12-15% compounding rate to meet a baseline retirement goal, Mutual Funds remain an unbeatable foundation. If you have the time for rigorous balance sheet analysis and thrive on active market participation, Direct Equity provides the necessary control over your growth engine.

However, the historical data is conclusive on one undeniable front: the highest sheer multiples of the last 15 years were not minted on the public stock exchange. They were secured by investors who traded temporary illiquidity for foundational, ground-floor entry prices. By buying the business before the investment bankers priced the IPO, they captured the absolute bulk of the wealth creation.

🤝Accessing Private Multiples with Altius

The unlisted space was an opaque, paper-heavy arena dominated entirely by institutional capital, private equity giants, and ultra-high-net-worth families. Information asymmetry was a feature, not a bug, designed to keep retail investors buying at retail prices while institutions bought wholesale.

This exact disparity is why Altius Investech exists.

We view our role not just as facilitators, but as the bridge between public market stability and pre-IPO explosive growth. By providing transparent data and highly secure execution, we have completely modernised this ecosystem.

The smartest capital doesn’t wait for the opening bell. It takes a definitive position while the story is still being written.

📜 Disclaimer

(Data as of March 13th, 2026, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)