You joined a fast-growing startup. The ESOP grant looked life-changing. Then the company raised another funding round, the valuation surged, and an IPO seemed inevitable. So, when your vesting window opened, you exercised your options using borrowed money.

The IPO was supposedly six months away.

Two years later, the IPO is still “coming soon.” Meanwhile, the loan EMI and interest burden continue every month.

How India’s ESOP Boom Created a Financial Problem

Between 2019 and 2022, India’s startup ecosystem aggressively used ESOPs to attract and retain talent. During the funding boom, startup valuations kept climbing, liquidity looked inevitable, and employees increasingly treated ESOPs as near-term wealth instead of long-term compensation.

The numbers highlight how rapidly ESOP culture expanded:

- Indian companies spent nearly Rs. 15,000 crore on ESOP programmes in FY2024-25.

- ESOP liquidity events among unlisted startups increased significantly between 2023 and 2025.

- More than 9,200 employees benefited from startup buybacks in 2025 alone.

However, beneath the success stories lies a growing financial issue.

Many employees exercised their ESOPs using loans during peak valuation cycles. The assumption was simple: exercise now, hold for a few months, sell after IPO, repay the loan, and retain the upside.

The problem is that IPO timelines shifted dramatically after the funding slowdown.

Today, the average Indian startup often takes 10–12 years to reach public markets. Consequently, thousands of employees are now holding illiquid shares financed through debt while IPO timelines remain uncertain.

The Leveraged ESOP Trap Explained

The issue begins when employees decide to exercise vested ESOPs.

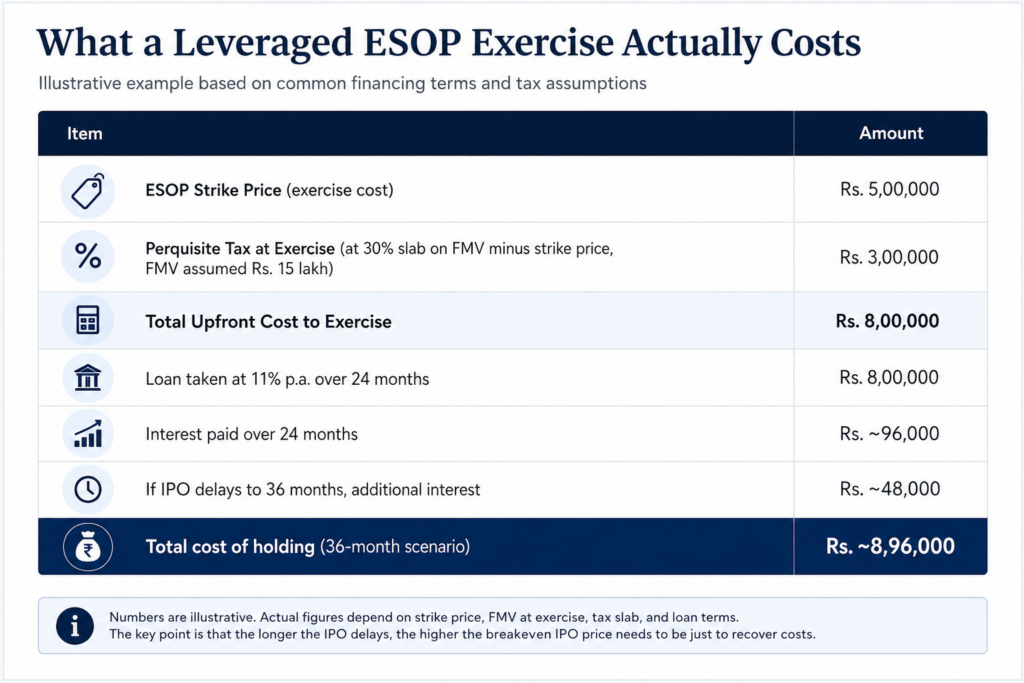

Although ESOPs provide the right to buy company shares at a fixed strike price, employees must still pay the exercise amount in cash. For late-stage startups, this upfront cost can easily range from Rs. 5 lakh to Rs. 30 lakh or more.

Because many employees lacked that liquidity, fintech lenders and ESOP financing platforms began offering specialised loans.

The logic initially appeared reasonable:

- Exercise the options.

- Wait for IPO or buyback.

- Sell shares at a higher valuation.

- Repay the loan.

This strategy works only if liquidity arrives on time.

Once IPO timelines get delayed by 12–24 months, the interest burden becomes substantial. As a result, employees start carrying both financial stress and illiquid equity simultaneously.

The ESOP Tax Problem Most Employees Underestimate

India’s ESOP taxation structure makes the situation significantly worse.

Tax Event 1: At Exercise

When employees exercise ESOPs, the difference between the Fair Market Value (FMV) and strike price is treated as salary income.This amount becomes taxable immediately, even if the employee has not sold any shares.

For example:

- Strike Price: Rs. 5 lakh

- FMV at Exercise: Rs. 15 lakh

- Taxable Perquisite: Rs. 10 lakh

An employee in the 30% tax bracket may immediately owe roughly Rs. 3 lakh in taxes without receiving any actual cash.

Tax Event 2: At Sale

The second tax event occurs when the shares are eventually sold.

- Shares held for over 24 months qualify for LTCG taxation.

- Shares sold earlier attract Short-Term Capital Gains tax.

The real danger emerges when startup valuations decline after exercise.In such cases, employees may have already paid high perquisite taxes based on inflated FMV calculations while the actual market value of shares later falls sharply.

This creates a permanent financial loss.

Why Former Employees Face the Biggest Risk

The situation becomes even harsher for employees who leave the company.

Most Indian startups provide a post-termination exercise window of only 30–90 days. Therefore, former employees must quickly decide whether to:

- Exercise the options using personal funds or loans

- Or allow years of vested ESOPs to expire completely

For many employees, taking a loan becomes the only realistic option.

However, once they leave the company, they lose visibility into IPO planning, internal liquidity discussions, and future buybacks. Consequently, they remain exposed to debt without any timeline certainty.

What Happens When the IPO Keeps Getting Delayed?

Employees holding leveraged ESOPs typically have four possible paths.

1. Wait for the IPO

This works only if the IPO arrives before loan pressure becomes unmanageable.

However, repeated delays increase interest costs and financial uncertainty.

2. Wait for a Company Buyback

Some startups conduct ESOP buybacks periodically.

Nevertheless, buybacks depend entirely on company decisions, board approvals, and available cash reserves. Employees cannot rely on them as guaranteed exits.

3. Sell Through ESOP Liquidity Funds

SEBI-registered AIFs and ESOP-focused liquidity platforms sometimes purchase vested shares directly from employees.

Although useful, these transactions often require company participation or founder approval.

4. Sell Shares in the Unlisted Secondary Market

This has become one of the most practical liquidity solutions for exercised ESOP holders.

Employees can directly sell their shares to interested investors through the unlisted secondary market without waiting for an IPO.

Most importantly, this route immediately converts illiquid equity into usable cash.

How the Secondary Market Solves the ESOP Liquidity Problem

The unlisted secondary market allows employees to sell exercised shares directly to investors interested in pre-IPO companies.

Unlike IPOs or company buybacks, secondary transactions do not depend on corporate events.

This makes the process significantly faster and more flexible.

Why Employees Use the Secondary Market

Immediate Liquidity

The primary objective for most leveraged ESOP holders is stopping the interest burden.

Receiving liquidity today at a moderate discount is often financially better than waiting years for an uncertain IPO.

No IPO Dependency

The company does not need to go public for shares to be sold.

As long as there is investor demand, employees can exit independently.

Legal and SEBI-Compliant

Once exercised, ESOP shares become ordinary equity shares. Therefore, they can legally be transferred through compliant unlisted market transactions.

Access to Active Investors

Pre-IPO investors actively seek stakes in recognised startups such as:

- Zepto

- PhonePe

- Flipkart

- Meesho

- Other late-stage venture-backed companies

Consequently, liquidity often exists even before IPO discussions formally begin.

How Altius Investech Helps ESOP Holders

Altius Investech: ESOP Liquidity Solution

Altius Investech operates as an active market maker in India’s unlisted shares market.

For ESOP holders facing loan pressure or uncertain IPO timelines, the platform facilitates secondary market liquidity through direct investor access.

What the Process Solves

- Converts exercised ESOPs into cash

- Helps employees repay loans faster

- Removes dependency on delayed IPOs

- Provides faster settlement and transaction support

- Assists with documentation and compliance processes

For many employees, the key decision is no longer maximizing valuation. Instead, it becomes reducing financial risk and eliminating accumulating interest costs.

Pricing Reality in the Secondary Market

Unlisted shares generally trade at a discount to the latest funding round valuation.

This discount reflects:

- Illiquidity risk

- Longer holding periods

- Lack of public market pricing

However, for many leveraged ESOP holders, waiting longer may create larger financial losses than accepting a moderate secondary-market discount today.

Therefore, the better question is often:

“Does selling now leave me financially better off than continuing to wait?”

In many delayed IPO situations, the answer becomes yes.

Final Analysis

ESOPs remain one of the strongest wealth-creation tools in India’s startup ecosystem.

When successful, they create extraordinary outcomes. Companies like Swiggy, Zomato, and Meesho generated substantial employee wealth through liquidity events and IPOs.

However, startup valuations are not the same as realised wealth.

An IPO is not guaranteed. Funding round valuations are not cash. And leveraged ESOP positions can become serious financial liabilities when liquidity timelines shift.

For employees carrying loans against exercised options, the secondary unlisted market provides a practical alternative.

It may not deliver the perfect valuation.

But it delivers something far more important: liquidity, certainty, and an exit path that does not depend on waiting endlessly for a future event that may continue getting delayed.

SELL YOUR ESOP SHARES THROUGH ALTIUS INVESTECH

We are active market makers in unlisted shares and work with ESOP holders across India’s leading startups to provide fast, legal, and fair secondary market liquidity.

For any query or personal assistance, feel free to reach out at support@altiusinvestech.com or call us at +91-6289225026

Learn more about Unlisted Companies and Pre-IPO opportunities at Altius Investech.

Join our LinkedIn Newsletter: The Market Buzz by Altius