MSEI was built to break the NSE-BSE duopoly. It nearly died trying. Now, with ₹1,240 crore in fresh capital from Groww, Peak XV, and Rainmatter and equity trading finally live. India’s most overlooked exchange is back in the conversation. The MSEI unlisted share price today sits around ₹4.5 – ₹5. Here is the complete story.

MSEI has spent seventeen years as a footnote now, launched with genuine ambition, crippled by scandal, starved of volumes, kept alive by its own treasury, and now quietly rebuilt with ₹1,240 crore of institutional capital, it is one of the most unusual stories in Indian financial markets.

Origin: MCX-SX and the Dream of a Third Big Exchange

Metropolitan Stock Exchange was not always called Metropolitan Stock Exchange. It began in 2008 as MCX Stock Exchange promoted by Jignesh Shah, the entrepreneur behind Multi Commodity Exchange of India (MCX). Shah had already built MCX into India’s dominant commodity exchange. The logic for a new stock exchange was straightforward: India’s equity markets were a two-player game. NSE dominated trading. BSE had legacy and listings. Neither faced any real competition. Transaction fees were high. Technology innovation was slow. Retail access remained limited. MSEI (then MCX-SX) was built to change that.

What MSEI Actually Set Out to Do

The exchange launched Currency Derivatives operations in October 2008, under the dual regulatory framework and was the first exchange to do so. It received full SEBI recognition as a stock exchange in December 2012. By February 2013, it had launched:

- Capital Markets segment (equity trading)

- Futures & Options segment

- Flagship index SX40 – a free-float weighted index of 40 large-cap stocks across diversified sectors

- SXBANK -a 10-stock banking sector index

Trading in equity and derivatives began on February, 2013.

On paper, MSEI had a full product suite, institutional-grade technology, and a credible promoter.

The NSEL Disaster and the Fall From Grace

The Scandal That Wasn’t MSEI’s But Destroyed It Anyway

In July 2013, the National Spot Exchange Limited (NSEL) collapsed in a ₹5,600 crore payment default scandal. NSEL was a separate entity not MSEI. But it was promoter-linked to Jignesh Shah. The fallout was immediate and catastrophic. Shah was arrested. His entire corporate ecosystem came under regulatory scrutiny. Institutional investors who had backed MCX-SX pulled back. Brokers who had signed up as members quietly redirected their technology and capital back to NSE. The credibility that a new exchange needs in its formative years, credibility that takes years to build and minutes to lose was gone.

The NSE Predatory Pricing Case

MSEI filed a ₹856 crore predatory pricing complaint against NSE at the CCI, alleging NSE had offered zero transaction fees in currency derivatives specifically to kill MSEI’s volumes. The CCI found NSE guilty, but the case has dragged through NCLAT for years with no resolution. The legal win exists on paper. The damage to MSEI was already done.

The Long Stagnation: 2015–2023:An Exchange Earning More From Its Savings Account Than Its Trading Platform

For nearly a decade, MSEI existed in a strange kind of limbo – licensed, regulated, technically operational, but economically invisible.

The exchange had a trading platform. It had indices. It had member brokers. What it didn’t have was traders. Without the NSE-linked predatory pricing case resolved, without a credible promoter at the helm post the NSEL scandal, and without any major broker integrating MSEI into their platforms, volumes on the exchange were negligible. Days would pass with near-zero equity turnover. To stay alive, MSEI did what any capital-heavy institution does when its core business stalls: it lived off its balance sheet. The exchange had raised significant capital in its early years and that money, parked in fixed deposits, corporate bonds, and liquid investments, was generating more income than the exchange itself.

The MSEI Unlisted Share Price in This Period traded between ₹1- ₹2 per share. Zero catalysts. Minimal volumes. Regulatory uncertainty. The MSEI unlisted share price was exactly where the business deserved to be.

The 2024–25 Revival: Smart Money Enters

Groww, Rainmatter, and Peak XV and other institutions Started Writing Cheques

The story changed in late 2024. And it changed because of who showed up — not what the financials said.

In December 2024, MSEI’s board approved a private placement raising ₹238 crore. The investors were:

- Billionbrains Garage Ventures the parent company of Groww, India’s largest retail broking platform

- Rainmatter Investments the investment arm of Zerodha’s founder, Nithin Kamath.

- Share India Securities a leading prop-trading and broking firm

- Securocrop Securities India

Then came the second, larger round. In August 2025, MSEI raised ₹1,000 crore through a fresh private placement. Investors included: Peak XV Partners, Jainam Broking, Trust Investment Advisors and others. Total capital raised: ₹1,240+ crore across two rounds.

This was not passive financial investment. Groww and Rainmatter are active participants in India’s trading ecosystem. They have direct relationships with retail traders, the technology infrastructure to onboard them onto new platforms, and a direct financial incentive to make MSEI succeed because they now own a piece of it. The metropolitan stock exchange share price in the unlisted market responded immediately. From ₹1–2, the MSEI share price in the grey market ran to ₹12–13 per share.

The Regulatory Speed Bump That Nobody Expected

A Single SEBI Circular Changed Everything

MSEI’s re-entry strategy was built around a tactical differentiation: Friday expiries for its SX40 index derivatives the one weekday left unclaimed by NSE and BSE.The plan was logical, Clean, Well-timed. Then SEBI moved the goalposts.

In May 2025, SEBI restricted all equity derivatives weekly expiries to just two days Tuesdays and Thursdays. No other days permitted, effective September 1, 2025. NSE kept Nifty 50 on Tuesdays, BSE kept Sensex on Thursdays and MSEI had nowhere to go.

Without a separate expiry day, SX40 derivatives would compete head-on against India’s two most liquid indices, on the same day as one of them, with zero existing open interest, zero broker integration on major platforms like Zerodha, Upstox, or Groww, and zero retail trader familiarity. As SEBI restricted weekly expiry contracts to limited days, investor sentiment quickly soured. MSEI price corrected sharply, losing nearly 65-70% of its peak value by mid-2025. As of mid-2025, the MSEI unlisted share price was trading in the ₹3–₹5 range.

Where MSEI Stands Today

On one side: a genuinely strengthened balance sheet, serious institutional backers, a live equity trading platform, and a SEBI-recognised exchange license that carries real scarcity value.

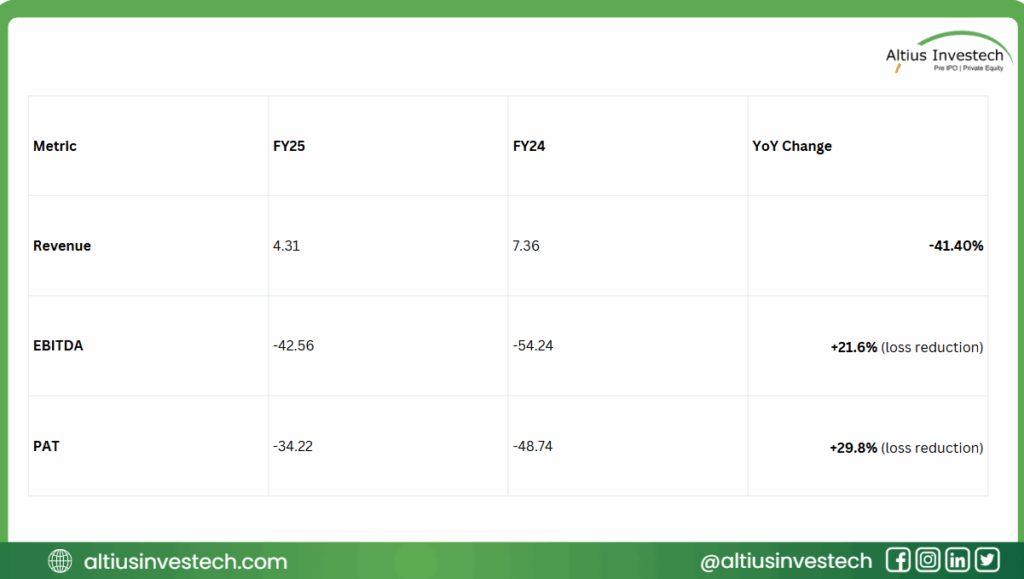

On the other: negligible trading volumes, no profitable quarter in its history, a derivatives strategy that hit a regulatory wall before it could prove itself, and a core revenue line actual exchange operations that generated just ₹4.31 crore in all of FY25.

Equity Trading: Finally Live, Still Early

MSEI’s equity trading launched with 130 stocks under a Liquidity Enhancement Scheme, with dedicated market makers providing two-way quotes to seed activity. The anticipated structural changes from the introduction of a new exchange are still playing out. The exchange is SEBI-licensed for Currency Derivatives, Equity, Equity Derivatives, Debt, and SME platform. The Liquidity Enhancement Scheme was introduced in January 2026, aligned with SEBI guidelines, to address low liquidity in the equity segment.

Conclusion

MSEI’s story is not a success story or a failure story. It is an unfinished story.

A bold start. A scandal that wasn’t its own but destroyed it anyway. A decade of irrelevance. A credible revival backed by India’s sharpest capital markets minds. And a regulatory wall that arrived precisely when the comeback was gaining momentum The exchange has capital. It has a license. It has backers who know this industry from the inside.

What it still needs is volume. And volume, in exchange economics, takes time.

How to Invest in MSEI UNLISTED SHARE

Looking to invest in pre-IPO and unlisted opportunities like MSEI? Explore exclusive access at Altius Investech — India’s trusted platform for unlisted shares.

Subscribe to The Market Buzz by Altius Investech for updates

GET IN TOUCH WITH US: For any query or personal assistance, reach out at support@altiusinvestech.com or call +91-8240614850

📜 Disclaimer: Data as of March 2026, sourced from public filings, MSEI audited results (FY25), and Altius Investech platform. For educational purposes only. Not investment advice. Altius Investech is not a SEBI-registered advisor.